Innovation and China’s Global Emergence

edited by Erik Baark, Bert Hofman, and Jiwei Qian

ISBN: 978-981-325-148-9

published August 2021

Or read this open access web edition

Chapter 11

Global Value Chains and the Innovation of the Chinese Mobile Phone Industry

Yuqing Xing

Introduction

Innovation and new technology are primary driving forces of economic development. Constant innovation is indispensable for a developing country wishing to avoid the middle-income trap, to grow into a high-income country and eventually to become a catch-up industrialised economy. After the rapid economic growth of the last four decades, China now has a $14 trillion economy, second in size only to the US. Its GDP per capita is now about $10,000, more than ten times that when China started its revolutionary economic reform in 1978. Continuous technological innovation has contributed substantially to that economic miracle. The Global Innovation Index 2018, compiled by Cornell University, INSEAD and the World Intellectual Property Organisation, ranks China as one of the 20 most innovative economies in the world. China’s aggregate investment in research and development (R&D) rose steadily as its economy grew continuously. In 2017, Chinese R&D was equivalent to 2.13 per cent of its GDP, making China the second in the world in terms of R&D investment (Atkinson and Foote 2019). Several studies (for example, Wu 2011; Iida, Shoji and Yoneyama 2018) concluded that China’s R&D investment contributed substantially to the growth of the total factor productivity of the Chinese economy.

To date, China is the largest exporter not only of labour-intensive goods, such as shoes, clothes and toys, but also of personal computers, mobile phones, digital cameras and other information communication technology (ICT) products. Chinese manufacturing output has exceeded that of the US and has become the world No. 1 (West and Lansang 2018). In the world market for white goods, China’s Haier Group has emerged as a leading maker of electronic appliances, to the point where Haier is now recognised as a global brand. In the global market for personal computers (PC), the Chinese company Lenovo has surpassed Hewlett-Packard and Dell to rank No.1 with 24 per cent of the global market (IDC 2018). In the global mobile phone market, home-grown Chinese brands Huawei, OPPO and Xiaomi are now three of the top five global smartphone brands (Counterpoint 2019b). Those achievements are largely the result of Chinese firms’ constant endeavours to innovate.

There are many channels in which Chinese firms can innovate, thus strengthening their competitiveness in global markets and narrowing technological gaps with foreign multinational corporations (MNCs) currently leading in both technology and brands. R&D investment, foreign direct investment, innovation institutions, fiscal subsidies, learning by doing and reverse engineering are all effective tools for innovation and product enhancement. In this chapter, I focus on the role of global value chains (GVC) in facilitating both product and process innovation of Chinese firms.

With the unprecedented trade liberalisation and the modularisation of the production processes of manufactured products, in particular ICT, MNCs have reorganised their production along GVCs, where specific activities and production tasks are standardised and allocated to firms in dispersed geographic locations as a result of outsourcing or offshoring. Participating in GVCs led by MNCs having advanced technology, internationally recognised brands and global distribution networks, offers Chinese firms opportunities to learn and to access new knowledge and advanced technology, thus enhancing their innovation capacity. The expansion of GVCs has been driven by production fragmentation and the modularisation of production tasks, the two factors that have lowered technical barriers to entry into technology-intensive industrial sectors. Taking advantage of the availability of standardised technology platforms, Chinese firms have concentrated on incremental, rather than drastic innovations, and have aimed at the introduction of differentiated products and at competition with leading foreign companies in both domestic and foreign markets.

To a certain extent, Chinese firms in the ICT industry achieved their success by adopting the value chain strategy. Most of China’s high-technology exports are manufactured with imported core technology components and are built on the top of technology platforms provided by foreign MNCs (Xing 2014). Assembling mobile phones for foreign vendors remains a major task for many Chinese firms. In this chapter, I will use the case of the Chinese mobile phone industry to illustrate the importance of GVCs in the facilitation of innovation, and demonstrate how Chinese firms have enhanced their innovation capacity by participating in GVCs.

GVCs, Innovation, and Upgrading

GVCs represent a new form of business operation, spanning multiple countries to create goods and deliver them to end consumers in world markets. Production fragmentation and modularisation enable production processes to disseminate ready-to-use goods, particularly ICT products, across geographically dispersed locations. Unprecedented liberalisation of trade and investment, innovation in ocean transportation and profit-seeking behaviour of MNCs have been the main drivers of the emergence of GVCs in recent decades (OECD 2013). Today, most manufacturing commodities are actually produced and traded along value chains. A typical GVC orchestrates a series of tasks necessary for delivery of a product. Ranging from conception to the delivery to end consumers, these tasks include research and development, product design, manufacture of parts and components, and assembly and distribution (Gereffi and Fernandez-Stark 2011: 4). Firms in different countries work in coordination to complete those tasks. Each firm specialises in one or more tasks in which it has comparative advantage, and contributes part of the whole value added of the final product. GVCs characterise a new division of labour—vertical specialisation across the provision of a single product. This specialisation is different from that in which firms make different products, as analysed by the British economist David Ricardo two centuries ago. Compared to conventional specialisation in different products, specialisation in tasks along value chains further refines the division of labour between nations and enhances the efficiency of resource allocation, consequently raising the productivity and economic growth of all economies involved. Three terms, GVC, supply chain and production network, refer interchangeably to the same phenomenon. Economists generally prefer the term GVC, because they are interested in the creation of value added and its distribution along value chains. Use of the terms “supply chain” and “production network” typically focuses on the production stages within value chains, the former emphasising who produces what, and the relations between upstream and downstream firms; the latter pays attention to the geographic locations of firms.

A lead firm, which manages the operation of a value chain and decides the relations between firms participating in the chain, is necessary for any meaningful GVC. If we break down the tasks contributing to the production of a product, from supply of the raw materials, to manufacture of the product and on to the eventual delivery of the product to targeted consumers, we can easily sketch a chain that superficially links all of the firms involved in the process. If the links along a value chain are not bound by binding contracts, that is if the relations are simply defined by free market transactions as buyer-seller relations, those value chains add little in terms of innovation. According to their governance structure, GVCs can be classified into producer-driven and buyer-driven. GVCs led by technology leaders in capital-intensive industries such as automobile, aircraft, computer and semiconductor, are producer-driven value chains. On the other hand, buyer-driven chains are typically organised by large retailers, branded marketers and branded manufacturers (Gereffi 1999: 41). The automobile value chains organised by Japanese auto-maker Toyota and the iPhone value chain of Apple are producer-driven GVCs. Similarly, Walmart, taking advantage of its extensive retail networks in the US and other countries, has built its buyer-driven GVC by sourcing all goods from some 60,000 contract manufacturers, 80 per cent of which are located in China.

Economists define innovation as the activities in which a firm applies new notions to the products, processes and other elements that generate increased value added. Innovation generally includes two dimensions: product innovation, the introduction of a new product; and process innovation, introduction of a new process for the manufacture or delivery of goods and services (Greenhalgh and Rogers 2010: 3ff.). It is critical to bear in mind that innovation is not a narrowly defined term referring to the creation of a drastically new product that surprises the world. To be sure, a completely new product such as the iPhone with its multi-touch screen and virtual keyboard is definitely a revolutionary innovation for the world. However, learning how to make smartphones with multi-touch screens is also an innovation for a firm imitating the iPhone. Most innovations are actually incremental achievements based on existing knowledge.

Innovations are not limited to new products, production processes or technology. New business models and marketing channels, aiming to enhance efficiency and value added, also constitute innovation. The OECD (2005) defines innovation as “the implementation of a new or significantly improved product (good or service), or process, a new marketing method, or a new organisational method in business practices, workplace organisation or external relations.” For instance, using iTunes to sell songs one by one, not combined in an album (which bundles popular and less-popular songs together) is a drastic innovation that has fundamentally changed the business model of the music industry. With iTunes, an artist can achieve fame and some financial success with just one hit song (Isaacson 2011).

Along GVCs, there are many tasks with varying degrees of technical sophistication. The value added created by those tasks also varies substantially. In general, product design, R&D, branding and retailing constitute relatively high value added, while assembly and production of standardised components contribute relatively low value added.

Firms from developing countries generally start with low value-added tasks such as assembly when they join value chains governed by foreign MNCs. Many Chinese firms started with assembly of mobile phones for foreign MNCs. Innovation is imperative for firms participating in GVCs if they wish to move up the value chain ladder and reach high value added. Otherwise, they may fall into a low value-added trap (Sturgeon and Kawakami 2010). Upgrading includes product upgrading (adding additional value to products); functional upgrading, such as from pure assembly to design work; and process upgrading (making a production process more efficient) (Morrison, Pietrobelli and Rabellotti 2008). Upgrading along GVCs and entering high value-added segments result from innovation activities.

GVCs: A New Path for Innovation by the Chinese

Mobile Phone Industry

In any value chain, the lead firm defines products, sets up quality standards and specifies technical parameters. All non-lead firms are obliged to follow the design rules specified by the lead firm. Intensive communication and information exchange between the lead firm and the suppliers are common, and offer a unique channel for non-lead firms to access new knowledge and production know-how. Learning mechanisms within GVCs include face-to-face interactions, knowledge transfer from lead firms, pressure to adopt international standards and training of the local workforce by lead firms (De Marchi, Giuliani and Rabellotti 2017). Gereffi (1999: 39) argued that participation in GVCs is a necessary step for industrial upgrading. Plugging into a GVC is similar to engaging in a dynamic learning curve. The transformation of some Asian suppliers from original equipment manufacturers (OEM) to original design manufacturers (ODM) in the apparel industry was significantly supported by their participation in apparel commodity chains.

China has for some time been recognised for its role as the assembly centre of major global brands. Before the emergence of smartphones, Motorola and Nokia used China as a major assembly base. Since the launch of the first generation iPhone, China has been the exclusive assembler of iPhones. At the peak, Samsung, the No. 1 mobile phone maker in the world, had 65% of its mobile phones assembled in China. The Chinese companies who assemble mobile phones for and supply components to those global mobile phone vendors are part of their value chains. The inter-firm linkages between the Chinese firms and upstream foreign buyers open the Chinese firms’ access to information about technology and consumer demand, and thus facilitate their innovation activities and upgrading progress along value chains.

Upgrading along value chains step by step from low value added to high value-added tasks constitutes a linear model of innovation. For instance, a firm starts from assembling mobile phones, then enters the manufacturing of components, and eventually produces mobile phones with its own brand. This is a linear path of innovation. It refers to a sequential upgrading along value chains and differs from the “linear model” that describes the process starting with basic research and then moving into stages of applied research, development and diffusion (Godin 2006). On the other hand, sourcing core technology from foreign suppliers and jumping directly to brand building lead to a non-linear model of innovation. Chinese original brand manufacturers (OBM), such as Xiaomi, OPPO and vivo, adopted the non-linear model by taking advantage of the modularisation of mobile phone production and successfully broke the monopoly of foreign rivals in both domestic and international markets.

To a large extent, the expansion of GVCs in ICT is attributed to the development of modularity, that is, the division of the manufacture of complicated products into modules or sub-systems that can be designed and manufactured independently. Modularity allows firms to mix and match components so as to produce final products catering to various consumer preferences. By exploring modularity in the design of products, firms can improve their product innovation rate (Baldwin and Clark 2018).

Firms in developing countries typically face two challenges: a technology gap and a market gap. A “technology gap”, the difficulty of accessing necessary technologies, is associated with weak innovation capacity (Schmitz 2007). Modularity creates the possibility of outsourcing essential technologies and enables firms in developing countries to specialise in value chain tasks in which they have comparative advantage. For example, a mobile phone consists of more than one thousand parts and components. The modularisation of mobile phone production has simplified the complexity of production and allowed potential entries to focus on non-core technology activities such as assembly. Given their relatively limited technology capacity in core components, say processors and memory chips, Chinese mobile phone makers entered the industry by sourcing core technological components from foreign MNCs and focusing on incremental innovations, marketing and brand building.

At the early stage of mobile phone development, their production was complicated and vertically integrated within a single firm. In that setting, a few large firms in industrialised countries (for example Nokia, Ericsson and Texas Instruments) monopolised global markets. In 2001 Wavecom, the French firm that first introduced the GSM model, developed the first module allowing handset makers to easily integrate applications into one main board. Taking advantage of this modularisation, China’s TCL, an electronic appliance maker, entered the mobile phone market (Sun, Chen and Pleggenkuhle-Miles 2010).

The “turnkey” solution introduced by Media Tek (MTK), a fabless Taiwanese semiconductor firm, is a milestone in the development of the Chinese mobile phone industry. It greatly enhanced the degree of the modularity of mobile phone production, especially for small phone makers who lack the required technology capacities. The turnkey solution, an integrated solution combining hardware and software, is a single chip that combines a baseband platform and multimedia (sound and image) data processing. Using the chip, firms can easily modify product functionality to appeal to preferences of diversified consumers, thus significantly lowering entry barriers (Imai and Shiu 2010: 21). MTK’s turnkey solution boosted the proliferation of “Shanzhai” mobile phone makers which had previously served as either OEMs or distributors for leading mobile phone brands. (“Shanzhai” originally meant counterfeit or imitation products.) However, a few studies have argued that Shanzai phones signified indigenous innovation products by small phone makers, and constituted good enough products at affordable prices to meet the needs of targeted customers. Shanzai phone makers gained market share not through technology innovation, but by adopting a novel business model (Hu, Wan and Zhu 2011).

In the age of smartphones, Android operating system (OS) and Qualcomm processor chipsets have become standard technology platforms. Leading Chinese smart phone makers ZTE, Xiaomi, OPPO and vivo all have adopted Android OS for their smartphones. Xiaomi and OPPO built 70 per cent of their phones on Qualcomm’s platforms; ZTE and vivo used Qualcomm’s platforms for 50 per cent and 60 per cent of their phones, respectively (World Bank 2019: 87). The Android OS platform has lowered technology barriers both for brand vendors, who were not capable of high-end product development, and for some handset assemblers, who were capable only of manufacturing white-box phones; this has facilitated the transformation of a few firms, OEMs, into original brand manufactures; OPPO is a noticeable example (Chen and Wen 2013: 10). The complexity of today’s technology platforms and the demand for product differentiation have enhanced communication and cooperation between foreign suppliers of technology platforms and the downstream Chinese firms using those platforms, thus facilitating innovation by Chinese mobile phone makers. For instance, as the major platform supplier to leading Chinese mobile phone makers, Qualcomm welcomed the research teams of those Chinese firms to its headquarters for product development. After intensive interactions with Qualcomm and power chip provider Texas Instruments, OPPO introduced the world’s first VOOC (Voltage Open Loop Multi-step Constant-Current Charging) system for smartphones (Humphrey et al. 2018).

In addition, the huge Chinese market, with a population of 1.4 billion, is conducive to marketing-focused strategies based on borrowed technology. In China a focus on the domestic market lessens the marketing gap and leads Chinese mobile phone makers towards a focus on marketing and product differentiation. Compared with leading foreign mobile phone makers, Chinese mobile phone makers have relatively more information and a better understanding of Chinese consumers. At the early stage of their development, Chinese mobile phone makers primarily adopted a low price strategy to attract consumers who could not afford expensive foreign brands, and targeted consumers in the country’s third and fourth tier cities, to which foreign brand vendors had paid less attention. In addition, the Chinese makers explored niche markets, introducing a variety of peripheral functions, such as dual SIM cards, selfie applications and long life batteries.

Brandt and Thun (2010) expected that, by adopting a value chain strategy, Chinese handset makers “will be more akin to a Dell (which does little product research and design) than Tom Watson’s IBM (which was highly vertically-integrated)”. However, Xiaomi’s MIU interface, OPPO’s VOOC flashing charging technology and Huawei’s Kirin processor provide clear evidence that they are technologically innovative. More importantly, by focusing on marketing and brand building, Chinese mobile phone makers have nurtured their brands, which are now recognised not only by Chinese users but also by foreign consumers. For instance, Xiaomi has surpassed both Apple and Samsung and emerged as the most popular brand in India. Brand leadership can boost sales growth, profit margin expansion and pricing power, and affords Chinese mobile phone makers the power to lead the value chains of their products and capture relatively large shares of value added. The bottom line is that brand development is an effective strategy for product innovation.

The Rise of the Chinese Mobile Phone Industry

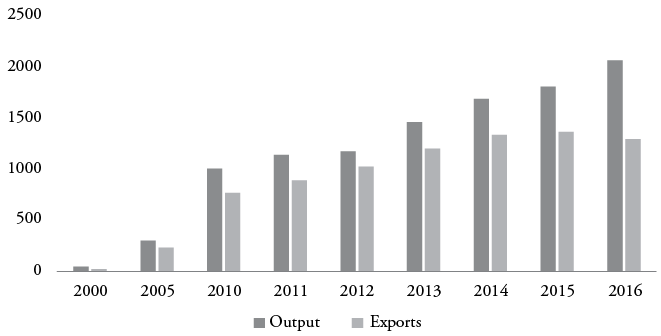

The rise of the Chinese mobile phone industry is a GVC success story. Despite its technological dependence on foreign technology platforms, this industry has emerged as the largest mobile phone producer and exporter in the world. Figure 11.1 outlines the trend of Chinese mobile output and exports from 2000 to 2016. At the beginning of the 21st century, the scale of China’s mobile phone output and export was relatively small. In 2000, China produced 52.5 million mobile handsets, of which 22.8 million, or about 43 per cent of the total, were exported to overseas markets. Driven by the drastic growth of global demand and rapid technology innovation in the sector, the annual output of mobile phones surged to 998.3 million in 2010. Exports grew even faster, jumping to 776 million that year, making China the No.1 exporter in the world. In 2016, China produced 2.0 billion mobile phones, of which 1.3 billion were destined for foreign markets.

Figure 11.1: Chinese Output and Export of Mobile Phones (million units)

Sources: UNCOMTRDE and China Statistics Bureau.

It is important to emphasise that, between 2005 and 2015, China’s mobile phone exports constantly accounted for more than three quarters of its annual output. At the peak, in the year of 2012, China shipped 1.03 billion mobile phones abroad, more than 87 per cent of the year’s output. Most of the exported phones were sold under foreign brands and Chinese brand mobile phones almost did not exist in international markets. This unambiguously demonstrates that the Chinese mobile phone industry was then functioning as the assembly centre of global mobile phone production. Participation in value chains governed by leading global vendors and performing assembly tasks were the main drivers of that growth. As a segment with numerous value chains, the Chinese mobile industry simultaneously benefited from the spillover effects of innovation and marketing activities of the leading global vendors, such as Apple and Samsung, which were steadily driving the global demand for mobile phones upward.

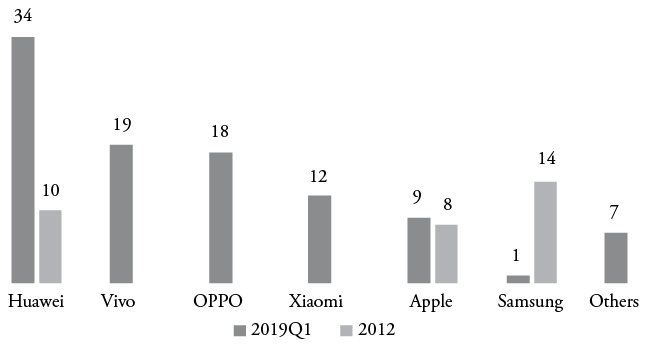

Surging output volume represents the quantitative dimension of China’s success in building its mobile phone production capacity. Another important dimension of that success is the brand development by indigenous Chinese firms. In addition to manufacturing handsets for foreign OBMs, the Chinese mobile phone industry successfully nurtured a few mobile phone brands which are competitive with foreign branded mobile phones in both China and abroad. Huawei, OPPO, vivo and Xiaomi, the most famous Chinese mobile phone brands, have successfully eroded the market share of their foreign rivals and reversed foreign domination of the sector completely in the Chinese market. Marketing research by Counterpoint (2019a) shows that in Q1 of 2019 Chinese brands captured 90 per cent of the Chinese smartphone market, led by Huawei with 34 per cent. The top four smartphone brands in terms of shipments (Huawei, vivo, OPPO and Xiaomi) together accounted for 87 per cent of the market, with Apple retaining a mere 9 per cent. The share of Samsung, the No. 1 mobile phone maker in the world, shrank to 1 per cent (Figure 11.2). Back in 2012, Samsung was the largest vendor in the Chinese market, with a 14 per cent market share, while Huawei had only 10 per cent. The market shares of OPPO, vivo and Xiaomi were negligible.

Figure 11.2: Chinese Smartphone Market Share (%)

Sources: Counterpoint (2019a) and Chen and Wen (2013).

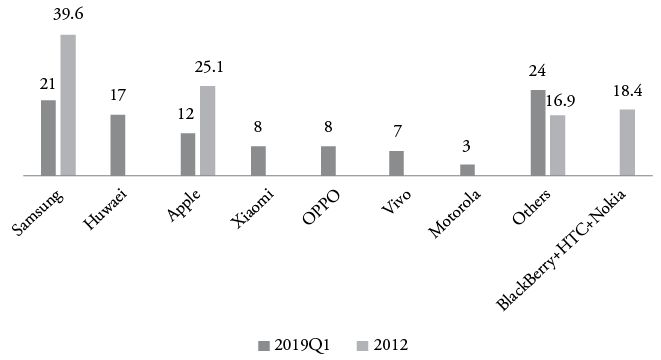

Building on their success in the home market, Chinese OBMs started to sell mobile phones with home-grown brands in international markets, gaining more and more market share, and eventually emerging as globally recognised brands. In Q1 of 2019, Huawei’s global market share was 17 per cent, surpassing that of Apple and ranking second, just 4 percentage points lower than Samsung. In fact, OPPO and vivo belong to the same company, BBK Electronics Corporation, a Chinese multinational firm. The combined market share of those two brands was 15 per cent, also exceeding that of Apple. In other words, BBK Electronics Corporation was actually the third largest mobile phone maker in the world. In 2012, Huawei’s market share was about one fourth of Samsung’s. OPPO, and neither vivo nor Xiaomi was known to foreign consumers. It is noteworthy that three bankrupted mobile phone makers, BlackBerry, Nokia and HTC, together accounted for 18.4 per cent of global shipments in 2012. At that time Chinese PC maker Lenovo acquired the Motorola brand. The market share of Motorola became part of the Chinese mobile phone makers’ share, so together those Chinese firms accounted for 44 per cent of smartphone shipments in the global market (Figure 11.3).

Figure 11.3: Global Smartphone Market Share (%)

Source: Counterpoint (2019b) and Chen and Wen (2013).

Moving Up in the iPhone Value Chain

The operation of Apple is an exemplary GVC. Apple has outsourced its production to contract manufacturers in various geographic locations and has concentrated mainly on product design, R&D and the development of software for its operating systems at one tail of the smile curve and marketing and retail at the other. All Apple products, iMac, MacBook Air, iPad and iPhone, are assembled in China. The phrase, “Designed by Apple in California. Assembled in China”, printed on the back of all Apple products, is a hallmark.

So far, Apple has released twelve generations of iPhones. With the introduction of the iPhone X, which carries most advanced technologies such as 3D sensing, but which comes with a $1,000 price tag, the iPhone has been transformed into a luxury high-technology gadget. China has been the exclusive assembly base for the iPhone since the first generation iPhone, iPhone 3G, was released in 2007. As the centre of the iPhone production, the Chinese mobile phone industry has benefited significantly from the popularity of the iPhone on the world market. Constantly rising global demand for it always automatically translates into demand for the services and periphery components supplied by the Chinese mobile phone industry. This has significantly promoted the growth of the Chinese sector in the last decades.

According to Xing and Detert (2010), Foxconn, a Taiwanese company with many production facilities in mainland China, received only $6.5 for assembling a ready-to-use iPhone 3G. That $6.5 accounts for 3.6 per cent of the total iPhone 3G manufacturing cost and roughly 1.3 per cent of the retail price. It consists of the whole value added captured by China in the process of manufacturing the iPhone 3G. To avoid the low-value added trap and take advantage of the learning opportunity offered by GVCs, upgrading and moving into relatively high value added segments are crucial for Chinese firms involved in the iPhone value chain. To assess this upgrading for participating Chinese firms, it is necessary to examine whether the number of Chinese firms involved in Apple’s value chains has increased, whether the range of tasks performed by Chinese firms has expanded and whether the technological sophistication of the tasks has risen.

Upgrading along the iPhone value chain is highly rewarding financially. In general, future uncertainty discourages firms from engaging in innovation efforts. Once a Chinese firm joins the army of Apple supplier companies, hundreds of millions of Apple users around the world will be potential customers for that firm’s products or services. The predictable and lucrative prospects motivate Chinese firms to raise the quality of their products to the standard of Apple. This is an example of innovation activities inspired by GVC participation. Grimes and Sun (2016) found that Chinese firms have played an increasingly important role in Apple’s value chains. In 2014, of 198 companies in the chain, 14 were Chinese. A few supplied core components, for example displays and printed circuit boards; this suggests that Chinese firms have strengthened their presence in the value chains controlled by Apple.

The teardown data of the iPhone X are examined so that the involvement of Chinese firms in the production of the iPhone X can be assessed. The teardown data, which provide detailed information about suppliers of the iPhone X as well as prices of parts and components, show that all core components embedded in the printed circuit board assembly (PCBA), including processor, DRAM, NAND, display and camera, are supplied by Apple, Qualcomm, Broadcom, Samsung, Toshiba, Sony and other non-Chinese companies. Indigenous Chinese companies manufactured only a small portion of non-core components. It should be noted that besides the assembler Foxconn, there are 10 local Chinese companies participating in the value chain of the iPhone X. Their tasks go beyond simple assembly and spread over relatively sophisticated segments. Table 11.1 lists Chinese firms and their corresponding tasks in the production of the iPhone X.

Table 11.1: Tasks Performed by Chinese Firms for the iPhone 3G and iPhone X

iPhone 3G (2009) | iPhone X (2018) |

• Assembly (Foxconn) | • Assembly (Foxconn); • Function parts for Touchscreen Module (Anjie Technology); • Filter for 3D sensing Module (Crystal Optech); • Coil Module for wireless charging (Lushare Precision); • Printed Circuit Board (M-Flex); • Speakers (Goertek); • RF Antenna (Shenzhen Sunway); • Battery Pack (Sunwoda); • Glass cover (Lens Technology); • Stainless Frame (Kersen Technology); • Camera Module (O-Filem) |

Source: Xing (2020).

Sunwoda, a leading Chinese battery maker, supplies the battery pack. Sony batteries were used in the early models of the iPhone; Sunwoda’s supplanting Sony as a battery pack supplier is a significant upgrading of Sunwoda along the iPhone value chain. Kersen Technology provides the iPhone stainless frames, and Lens Technology manufactures the glass covers. The stainless frame and glass back cover together cost $53, about 13 per cent of the total manufacturing cost and more than 11 times the assembly fee of $4.5. The iPhone X is the first iPhone with a glass back cover. In addition, Chinese companies Anjie Technology and Lushare Precision are involved in manufacturing iPhone X touch screens and 3D sensing modules respectively. Touch screens and 3D sensing modules are critical technological components of the iPhone X. The former translates users’ finger movements into data that can be interpreted as commands, while the latter is a key element of the facial recognition system, a new feature introduced in the iPhone X. Chinese company Dongshan Precision joined the suppliers to Apple by acquiring American company M-Flex; it now supplies the printed circuit boards for the iPhone X for $15 per unit. Chinese companies Goertek, Shenzhen Sunway, Crystal-Opetch and O-film provide functional parts: speakers, RF antennas, filters and camera modules respectively. The involvement of those Chinese firms, even though in non-core technology segments of the Phone X value chain, indicates that the Chinese mobile phone industry as a whole has moved to the upper rungs of the iPhone value chain ladder. According to the teardown data, the total bill for materials of the iPhone X is $409.25, of which the Chinese firms jointly contribute $104, about 25.4 per cent of the total manufacturing cost.

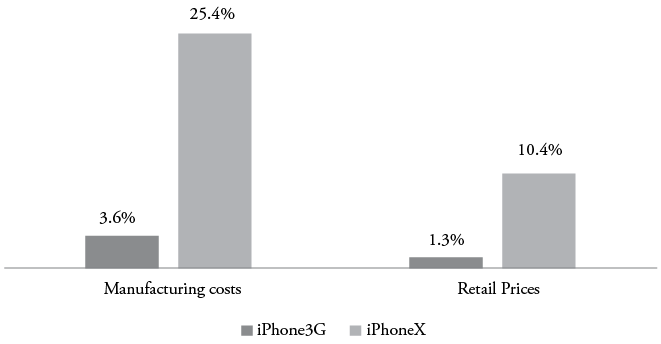

A complete value chain consists of pre-production, production and post-production activities. For estimation of the domestic value added in a country’s exports, and to fairly evaluate bilateral trade balances with its trading partners, the manufacturing cost of a product can appropriately be used as a benchmark. For assessment of the value captured by Chinese firms in the whole iPhone X value chain, we should go beyond production and use retail price as a benchmark, since it proxies total value added of the iPhone X. We found that the Chinese firms together captured 10.4 per cent of the value added in the iPhone X’s retail price $1,000, much higher than that for iPhone 3G (Figure 11.4).

Figure 11.4: Chinese Value Added Embedded in the iPhone 3G and iPhone X

Source: Xing and Detert (2010) and the author’s calculation.

Therefore, compared with the production of the iPhone 3G, more Chinese firms are involved in the production of the iPhone X and they perform more diversified tasks and capture higher value added. This implies significant upward movement by Chinese firms along the iPhone value chain. All of Apple’s suppliers are required to satisfy the high quality and technology standards defined by it. The pressure to meet these standards facilitated the upgrading process of those firms and their innovation activities.

OPPO and Xiaomi: a GVC Success Story

OPPO is one of the most popular mobile phone brands in the Chinese market. In the first quarter of 2019, it ranked No. 3 after Huawei and vivo, with an 18% market share (Counterpoint 2019a). “Designed by OPPO Assembled in China” is printed on the back of OPPO phones. The statement, actually an imitation of the similar phrase on the back of the iPhone, sounds a little bit strange, as OPPO is clearly a 100 per cent Chinese company. OPPO intends to use the statement to convey a message to its users: OPPO phones use state-of-the-art technologies and China’s role is limited to assembly. The statement is self-evident that OPPO phones are products of GVCs. By providing an excellent selfie experience, OPPO smartphones have achieved widespread popularity, particularly among younger consumers. OPPO actually markets its phones as camera phones in commercials, to differentiate its brand from others. The company operates a nationwide network of 200,000 stores to sell its products in China. It generally pays a much more generous commission than the industrial average to motivate its salespersons (Wang 2016). Globally, OPPO shipped 25.7 million smartphones in the first quarter of 2019 and held fifth position among leading mobile phone vendors (Counterpoint 2019b).

To understand the dependence of OPPO on foreign technology platforms, the teardown data of the OPPO R11s, a premium smartphone released in 2017 and which runs on Android OS, are used to examine the suppliers of OPPO in detail. The teardown data show that all core components were sourced from foreign suppliers. The phone is powered by Qualcomm’s mid-range Snapdragon 660 processor, coupled with an embedded multi-chip package (eMCP) by Samsung. It features a 6.1-inch full screen AMOLED display by Samsung. All components embedded in the PCBA are supplied by foreign companies, particularly Qualcomm, Samsung, TDK and Muruta. SONY supplies the rear camera, Samsung the front camera for selfies. The total value added of foreign companies accounts for 83.3 per cent of the total manufacturing costs, consistent with the statement “assembled in China” (Table 11.2). A few Chinese firms provide a limited number of non-core components such as the fingerprint module (by O-film) and the battery (by Sunwoda).

Table 11.2: Foreign Technology and Suppliers of the OPPO R11s

Component | Supplier | Total Foreign Value Added |

Operating System | Android (US) | 83.3% of the total manufacturing cost $293.18 |

CPU: | ||

Snapdragon 660 | Qualcomm (US) | |

Memory: eMCP | Samsung (Korea) | |

Display: | ||

6.01inch, 1080x2160 pixels | Samsung (Korea) | |

Dual Camera | Sony (Japan) | |

Front Camera | Samsung (Korea) |

Source: Xing and He (2018).

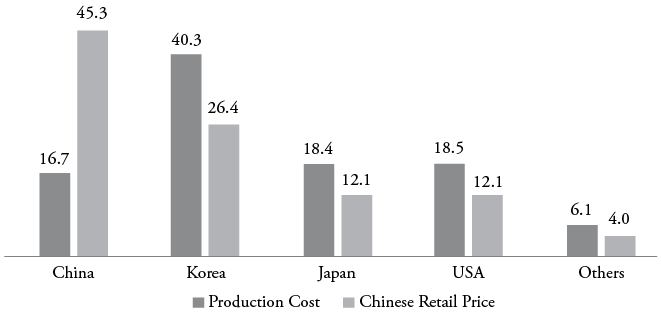

Figure 11.5 shows the estimated distribution of value added of the OPPO R11s by country. The total bill for the phone’s materials is $293.18. Korean companies Samsung and Hynix together contributed 40.3 per cent of the total manufacturing cost. The second largest source of value added is 18.5 per cent, from the US. The contribution of the Japanese companies Sony, Muruta and others is estimated at 18.4 per cent, almost the same as that of the US. The Chinese companies accounted for the smallest share of value added. However, if we take the retail price of 2999 RMB as a benchmark, the cross-country distribution of value added is dramatically different: China emerges with the largest share of total value added, about 45.3 per cent of the retail price, which shows the power of brand ownership: that significantly high share is attributed to brand value and the corresponding retail service (Figure 11.5).

Xiaomi is the 4th largest mobile phone maker in the world. It shipped 27.8 million smartphones globally in 2019 (Counterpoint 2019b). Unlike OPPO, Xiaomi is a factory-less maker and has no assembly facilities. It outsources the production of its phones to contract manufacturers. Xiaomi is the first Chinese mobile phone vendor to sell phones exclusively online. The secrets of Xiaomi’s success include: selling a premium phone at about a half the price of its competitors; fast-flashing sales; and nurturing a community of users. Xiaomi’s largest foreign market is India, where it surpassed Samsung to become the No.1 smartphone vendor.

Similar to OPPO smartphones, all Xiaomi phones run on Android OS and are designed based on Qualcomm chipsets. Xiaomi, however, has developed a unique MIUI interface based on Android OS and installed it on Xiaomi phones to differentiate it from other brands. The case of the flagship device MIX 2 released in the second half of 2017 demonstrates Xiaomi’s reliance on foreign technology. The teardown data of the MIX2 reveal that it is powered by a top-end Qualcomm Snapdragon 835 processor, which costs $62.56, the most expensive part in the PCBA of the MIX2. It has a 6GB NAND flash memory, supplied by the Korean company Hynix, and 64GB Dynamic random access memory manufactured by Samsung. With regard to functional parts, the Xiaomi MIX 2 features a 5.99 inch 1080x2160 pixel display produced by Japan Device Inc. Sony supplies the camera embedded in the phone. Chinese companies are mainly involved in the provision of non-core components and services. For instance, BIYADI Electronics supplies the frame of the phone and the battery company SCUD provides the battery. Table 11.3 lists major foreign technology suppliers of the Xiaomi MIX 2.

Figure 11.5: Distribution of the OPPO R11s Value Added by Country (%)

Source: Xing and He (2018).

Table 11.3: Foreign Technology and Suppliers of the Xiaomi MIX 2

Component | Supplier | Total Foreign Value Added |

Operating System | Android (US) | 84.6% of the total manufacturing cost $335.98. |

CPU: | ||

Snapdragon 835 | Qualcomm (US) | |

NAND 6GB | Hynix (Korea) | |

DRAM 64GB | Samsung (Korea) | |

Display: | ||

5.99 inch, 1080x2160 | JDI (Japan) | |

Camera | SONY (Japan) |

Source: Xing and He (2018).

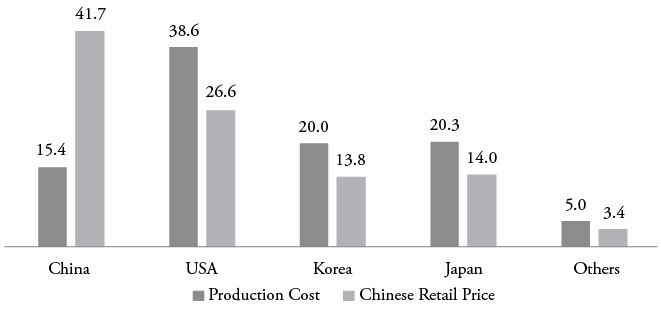

Foreign companies together accounted for 84.6 per cent of the value added in manufacturing the Xiaomi MIX 2 (Figure 11.6). Specifically, the US companies captured 38.6 per cent of the value added, the highest among all country groups, followed by Japanese companies with 20.3 per cent and Korean 20.0 per cent. Similar to the case of the OPPO R11s, the Chinese companies’ contribution to the value added of the MIX 2 is relatively small, about 15.4 per cent of total production cost, suggesting that the involvement of Chinese companies in the value chain of Xiaomi is limited. The retail price of the MIX is 3299 RMB. If we include the value added generated by Xiaomi’s brand and the retail service, the share of the Chinese value added is 41.7 per cent, significantly higher than that when only production is considered. Again, the brand ownership raises the Chinese value added.

Figure 11.6: Distribution of the Xiaomi MIX 2’s Value Added (%)

Source: Xing and He (2018).

The teardown data of the OPPO R11s and the Xiaomi MIX 2 suggest that foreign technology remains indispensable for Chinese brand mobile phones. Even though OPPO and Xiaomi have emerged as global brands, the innovations of the two companies are incremental and marginal. Instead of targeting drastic technology advancement for catching up, they emphasise product differentiation, brand building and a business model which takes advantage of the availability of the technology platforms. The successes of OPPO and Xiaomi indicate that GVCs provide non-linear models of how innovation and firms of developing countries can enter the high-tech industry and emerge as lead firms by sourcing necessary technologies.

The innovation path of Huawei differs from those of Xiaomi and OPPO. It is the largest mobile phone maker in China and the second largest in the world. Huawei was regarded as the most innovative Chinese company. In 2018, it invested $15.3 billion in R&D and even outspent Apple (Bloomberg 2019). Compared to those by OPPO and Xiaomi, Huawei’s innovations are relatively more technology-oriented. According to the teardown data of the Japanese firm Fomalhaut Techno Solution, Huawei P30 Pro is powered by the Kirin processor developed by HiSilicon, a subsidiary of Huawei, suggesting that Huawei has developed the technological capacity to design a chip set which can substitute for Qualcomm’s chipsets, currently adopted by most Chinese mobile phone makers (Table 11.4). The Kirin processor marks the highest level of technological innovation by the Chinese mobile phone industry. In addition, the Huawei P30 Pro incorporates an OLED display manufactured by Chinese company BOE Technology. The OLED display is the most expensive part embedded in the Huawei P30 Pro. Because of the above two key components, the Chinese value added in the Huawei P30 Pro reached 38.1 per cent, much higher than that in the OPPO R11s and the Xiaomi MIX 2. Samsung, LG and JDI have been dominant in the OLED display market. The adoption of BOE Technology’s OLED display by Huawei is a noticeable inroad into the monopoly of the foreign companies.

Table 11.4: Technology and Suppliers of the Huawei P30 Pro

Component | Supplier | Total Foreign Value Added |

Operating System | Android (US) | 61.9% of total manufacturing cost. |

CPU | HiSilicon (China) | |

NAND | Samsung (Korea) | |

DRAM | Micron Technology (US) | |

Display | BOE Technology (China) |

Source: Tanaka (2019).

Concluding Remarks

The rise of the Chinese mobile industry is impressive and unique. On the one hand, China has become the largest mobile phone maker and the largest exporter in the world. Of the top five global mobile phone brands, three are Chinese: Huawei, Xiaomi and OPPO. On the other hand, all Chinese smartphones depend on foreign technology platforms. They run on the Android OS owned by Google and are powered by Qualcomm chipsets. However, that technology deficiency has not hindered the emergence of the Chinese mobile phone industry. The value chain strategy of sourcing necessary technology platforms and concentrating on product differentiation and incremental innovation explains the significant achievement of the Chinese mobile phone industry. GVCs facilitated by modularisation provide a unique path for Chinese firms to enter the industry and leapfrog technological barriers. As latecomers, Chinese firms had to begin as contract manufacturers, assembling mobile phones for foreign vendors. The emergence of home-grown brands in global markets and their upgrading along the value chain of the iPhone suggest that Chinese firms are capable of moving to upper phases of value chain work, and that their innovative activities performed a critical role in successful competition with foreign rivals.

The development of GVCs makes it possible to achieve a non-linear model of innovation, although the GVC strategy is not risk-free. All the cases presented here refer to technology platforms owned by foreign companies, mainly the American companies Google and Qualcomm. The efficiency and effectiveness of the GVC strategy are based on the assumption that Chinese firms are able to purchase necessary technologies via fair market transactions. This assumption no longer holds.

As US-China trade evolved into a technology war, Huawei was banned by the Trump administration from purchasing chipsets manufactured by American companies. Even worse, the Trump administration further strengthened the technological sanctions on Huawei and barred any companies from using American technologies to produce chipsets for Huawei. This embargo simply announced the death of Huawei’s Kirin processors, which were manufactured by Taiwan Semiconductor Manufacturing Company with American technology. The technological decoupling between the US and China implies that the golden era of GVCs is over. National security has become a major obstacle for adopting GVC strategy. The Chinese mobile phone industry should invest in core mobile phone technologies and be prepared for a possible complete decoupling between the two countries.

References

Atkinson, Robert D. and Caleb Foote. 2019. Is China Catching Up to the United States in Innovation? Washington DC: Information Technology and Innovation Foundation. Available at http://www2.itif.org/2019-china-catching-up-innovation.pdf?_ga=2.

11950839.2136986670.1612821833-635563182.1612821833 [accessed 8 Feb. 2021].

Baldwin, Carliss Y. and Kim B. Clark. 1997. “Managing in an Age of Modularity”, Harvard Business Review, Sept.–Oct. Available at https://hbr.org/1997/09/

managing-in-an-age-of-modularity [accessed 25 Nov. 2020].

Bloomberg 2019. No Pay, No Gain: Huawei Outspends Apple on R&D for a 5G Edge. Available at https://www.bloomberg.com/news/articles/2019-04-25/huawei-s-r-d-spending-balloons-as-u-s-tensions-flare-over-5g [accessed 18 July 2019].

Brandt, Loren and Eric Thun. 2011. “Going Mobile in China: Shifting Value Chains and Upgrading in the Mobile Telecom Sector”, International Journal of Technological Learning, Innovation and Development 4, 1/2/3: 148–80.

Chen Shin-Horng and Wen Pei-Chang. 2013. The Development and Evolution of China’s Mobile Phone Industry. Working paper series No. 2013–1. Taipei: Chung-Hua Institute for Economics Research.

Cornell University, INSEAD and the World Intellectual Property Organization. 2018. The Global Innovation Index 2018: Energizing the World with Innovation. Ithaca, Fontainebleau and Geneva.

Counterpoint. 2019a. Chinese Smartphone Market Share by Quarter. Available at https://www.counterpointresearch.com/china-smartphone-share/ [accessed 11 July 2019].

________. 2019b. Global Smartphone Market Share by Quarter. Available at https://www.counterpointresearch.com/global-smartphone-share/ [accessed 11 July 2019].

De Marchi, Valentina, Elisa Giuliani and Roberta Rabellotti. 2018. “Do Global Value Chains Offer Developing Countries Learning and Innovation Opportunities?”, European Journal of Development Research 30, 3: 389–407.

Gereffi, Gary. 1999. “International Trade and Industrial Upgrading in the Apparel Commodity Chain”, Journal of International Economics 48, 1: 37–70. Available at https://www.soc.duke.edu/~ggere/web/gereffi_jie_june_1999.pdf [accessed 19 Feb. 2021].

Gereffi, Gary and Karina Fernandez-Stark. 2011. Global Value Chain Analysis: a Primer. Durham, NC: Duke University Center on Globalization, Governance and Competitiveness.

Godin, Benoît. 2006. “The Linear Model of Innovation: The Historical Construction of an Analytical Framework”, Science, Technology, and Human Values 31, 6: 639–67.

Greenhalgh, Christine and Mark Rogers. 2010. Innovation, Intellectual Property, and Economic Growth. Princeton, NJ: Princeton University Press.

Grimes, Seamus and Sun Yutao. 2016. “China’s Evolving Role in Apple’s Global Value Chain”, Area Development and Policy 1, 1: 94–112.

Hu Jin-Li, Wan Hsiang-Tzu and Zhu Hang. 2011. “The Business Model of a Shanzai Mobile Phone Firm in China”, Australian Journal of Business and Management Research 1, 3: 53–61.

Humphrey, John et al. 2018. “Platforms, Innovation and Capability Development in the Chinese Domestic Market”, The European Journal of Development Research 30, 3: 408–23.

IDC [International Data Corporation]. 2018. Lenovo Reclaims the #1 Spot in PC Ranking in Q3 2018. Available at https://www.businesswire.com/news/home/20181010005962/en/Lenovo-Reclaims-the-1-Spot-in-PC-Rankings-in-Q3-2018-According-to-IDC [accessed 8 Feb. 2021].

Iida Tomoyuki, Shoji Kanako and Yoneyama Shunichi. 2018. What Drives China’s Growth? Evidence from Micro-level Data. Bank of Japan Working Paper Series, No.18-E-19, November.

Imai Ken and Shui Jingming. 2007. A Divergent Path of Industrial Upgrading: Emergence and Evolution of the Mobile Handset Industry in China. IDE Discussion paper No. 125. Chiba: Institute of Developing Economies/ Japan External Trade Organization [IDE-JETRO].

Isaacson, Walter. 2011. Steve Jobs. New York: Simon & Schuster.

Morrison, Andrea, Carlo Pietrobelli and Roberta Rabellotti. 2008. “Global Value Chains and Technological Capabilities: a Framework to Study Learning and Innovation in Developing Countries”, Oxford Development Studies 36, 1: 39–58.

OECD. 2005. “The Measurement of Scientific and Technological Activities: Guidelines for Collecting and Interpreting Innovation Data: Oslo Manual, Third Edition” prepared by the Working Party of National Experts on Scientific and Technology Indicators, OECD, Paris, para. 146.

________. 2013. Interconnected economies: Benefiting from Global Value Chains. Paris: Organisation for Economic Cooperation and Development. Available at https://www.oecd.org/sti/ind/interconnected-economies-GVCs-synthesis.pdf [accessed 8 Feb. 2021].

Schmitz, Hubert. 2007. “Reducing Complexity in the Industrial Policy Debate”,

Development Policy Review 25, 4: 417–28.

Sturgeon, Timothy J. and Kawakami Momoko. 2010. Global Value Chains in the

Electronics Industry:

Sun Sunny Li, Chen Hao and Erin Pleggenkuhle-Miles. 2010. “Moving Upward in Global Value Chains: The Innovations of Mobile Phone Developers in China”, Chinese Management Studies 4, 4: 305–21.

Tanaka, A. 2019. “Teardown of Huawei Latest Model Shows Reliance on US Souring,” Nikkei Asia, 26 June 2019. Available at https://asia.nikkei.com/Economy/Trade-war/Teardown-of-Huawei-latest-model-shows-reliance-on-US-sourcing [accessed 2 Feb 2021].

Wang Yue. 2016. “OPPO Explained: How a Little-Known Smartphone Company Overtook Apple in China”, Forbes, 22 July 2016. Available at https://www.forbes.com/sites/ywang/2016/07/22/oppo-explained-how-a-little-known-smartphone-company-overtook-apple-in-china/?sh=41deb5b1393c [accessed 25 Nov. 2020].

Was the Crisis a Window of Opportunity for Developing Countries? Washington DC: The World Bank Policy Research Working Paper, No. 5417. Available at https://openknowledge.worldbank.org/bitstream/handle/10986/3901/WPS5417.pdf?sequence=1&isAllowed=y [accessed 8 Feb. 2021].

West, Darrell M. and Christian Lansang. 2018. Global Manufacturing Scorecard: How the US Compares to 18 Other Nations. Washington DC: Brookings. Available at https://www.brookings.edu/research/global-manufacturing-scorecard-how-the-us-compares-to-18-other-nations/ [accessed 25 Nov. 2020].

World Bank. 2019. Global Development Report 2019: Technological Innovation, Supply Chain Trade, and Workers in a Globalized World. Washington DC: World Bank.

Wu Yanrui. 2011. “Total Factor Productivity Growth in China, a Review”, Journal of Chinese Economic and Business Studies 9, 2: 111–26.

Xing Yuqing. 2014. “China’s High-Tech Exports: The Myth and Reality”, Asian Economic Papers 13, 1: 109–23.

________. 2020. “How the iPhone Widens the US Trade Deficit with China: The Case of the iPhone X”, Frontiers of Economics in China 15, 4: 642-58.

Xing Yuqing and Neal Detert. 2010. How the iPhone Widens the US Trade Deficit with China. Tokyo: ADB Institute Working paper 257.

Xing Yuqing and He Yuzhen. 2018. The Domestic Value Added of Chinese Brand Mobile Phones. Tokyo: National Graduate Institute for Policy Studies [GRIPS] Discussion Paper 18-09.