Innovation and China’s Global Emergence

edited by Erik Baark, Bert Hofman, and Jiwei Qian

ISBN: 978-981-325-148-9

published August 2021

Or read this open access web edition

Chapter 10

Industrial Policy and Competitive Advantage: A Comparative Study of the Cloud Computing Industry in Hangzhou and Shenzhen

Bai Gao and Yi Ru

The development of the digital economy has become a driving force behind China’s economic transformation. The share of the digital economy in China’s total GDP jumped from 26.1 per cent in 2014 to 34.8 per cent in 2018 (Yu and Dong 2019). The cloud computing industry, an important segment of the digital economy, grew very rapidly. Between the first quarters of 2018 and 2019, the Infrastructure as a Service (IaaS) segment of the cloud computing industry grew 74 per cent. China has become the second largest cloud computing market in the world, next only to the United States (Yiou 2019b). In 2018, four of the world’s top ten companies in the cloud computing industry were Chinese, with Alibaba at number three, Tencent at number six, China Telecom at number seven, and Kingsoft at number ten (IDC 2019).

Sustained by Alibaba and Tencent, Hangzhou and Shenzhen have emerged as two powerhouses in China’s cloud computing industry. Between April 2017 and the end of 2018, in the Chinese market the Ali Cloud grew 101 per cent, recorded $2.5 billion in revenue and was ranked number one (Alibaba Group 2018), while the Tencent Cloud grew 128 per cent (Yiou 2019a), recorded $1.4 billion in revenue and was ranked as number two. The Tencent Cloud’s rank in the global market jumped from number eighteen in 2017 to number six in 2018 (Gartner 2019).

Despite the rapid development of cloud computing in both Hangzhou and Shenzhen, we observe some distinctive variations between these two cities. First, Shenzhen adopted its first industrial policy to support cloud computing as early as 2010, while Hangzhou did not take action until 2013. Second, even though Shenzhen adopted an official policy for cloud computing earlier than Hangzhou, the goal it set up for the industry was relatively modest. In contrast, while Hangzhou was initially slow to support the industry, its support became quite aggressive from 2014 onwards. Third, although both cities adopted industrial policies to support cloud computing’s development, Shenzhen has treated it as merely one of several strategic industries while Hangzhou has regarded it as its number one priority. And indeed, in terms of market size, Hangzhou’s cloud computing industry has left Shenzhen’s behind.

To what extent can we use industrial policy to explain the development of the cloud computing industry in China? What kinds of industrial policy have Chinese local governments adopted to develop the digital economy? Is Chinese industrial policy different from that practised by governments in other countries? What are the implications of China’s industrial policy pertaining to the digital economy for the futures of both the Chinese and international economies?

We examine the impacts of Chinese industrial policy on the digital economy in relation to private entrepreneurship through an analysis of the development of the cloud computing industry in Hangzhou and Shenzhen, focusing on Alibaba and Tencent. We first review the existing literature on industrial policy and identify four types of states differentiated by the goals of their industrial policies: the “developmental state” that focuses on promoting high value-added industries, the “social protection state” with policies oriented towards restricting competition in order to maintain political stability, the “entrepreneurial state” that shoulders the burdens of investment risks in radical frontier technologies in an effort to spur innovations, and the “market facilitating state” that emphasises building infrastructure and reducing the transaction costs for private companies. Then we present a theory of the “competitive-advantage-building state”, informed by new structural economics and Michael Porter’s competitive-advantage diamond diagram but at the same time transcending both of them in important ways.

Contrary to the stereotype of the heavy-handed Chinese state, we argue that the competitive-advantage-building state in the digital economy focuses on enhancing factor endowment, building infrastructure, reducing transaction costs, creating market demand, encouraging industrial clusters and promoting corporate rivalries. The primary goal of industrial policy practised by the competitive-advantage-building state is to create favourable structural and institutional conditions that empower private companies in market competition. It identifies technological frontiers and adopts industrial policies to lure private investments towards them. Instead of leading the breakthrough from 0 to 1, however, the state has emphasised pushing commercialisation forward from 1 to 100. Such an industrial policy is often informed by private entrepreneurship and constrained by the dominance of private companies in the digital economy. The policy’s effectiveness is often determined by private companies’ willingness to follow the state’s guidance.

The Developmental State

Classical industrial policies were practised by the developmental states of Japan and South Korea during their high-speed economic growth in the 1950–70 period. The state targeted high value-added industries in which domestic companies had not yet obtained competitive advantage in an effort to obtain more trade benefits through exports. In order to nurture domestic companies’ competitiveness in these industries, the state established trade barriers, both in tariff and non-tariff forms, and allocated the country’s limited resources to these industries (Johnson 1982; Gao 1997). The developmental state in Japan encouraged oligopolistic competition: its rationale was that too many players in the same industry would result in “excessive competition” thereby dispersing limited resources and preventing domestic companies from becoming big players. Without competition, however, domestic companies would never become competitive in international markets. In practice, the Japanese state never controlled all industries. Rather, it cared only about the strategic ones (Gao 1997, 2001).

The Social-Protection State

The social-protection state considers political stability its major policy objective. Its industrial policy is carried out in sunset industries where domestic companies have lost comparative advantage. A major character of this type of industrial policy is its restriction on competition (Tilton 1996; Uriu 1996). For this reason, some analysts called it “competition policy”. Many countries practise this type of industrial policy because, by controlling competition, it prevents massive layoffs and reduces the burden of social protection by the state. To protect jobs and slow down the decline of sunset industries, the state in both Japan and in Europe exerted various industry-based anti-competition regulations and some countries even allowed medium-size and small companies to organise cartels during recession (Gao 2001; Tilton 1996). In China, undertaking a new pattern of industrial governance after the reform started, the state often practised anti-competition policy, constraining market entry and exercising frequent administrative interventions (Chen Qingtai 2016; Wu Jinglian 2016).

The Entrepreneurial State

The entrepreneurial state is represented by the Defense Advanced Research Projects Agency (DARPA), a part of the US federal government’s Department of Defense (Mazzucato 2015). Its industrial policy aims to reduce the enormous risks associated with investment in R&D in radical frontier technologies in order to spur innovation. Contrary to the conventional image of the United States in which private companies play the leading role in technological innovation, the US federal government “has provided early-stage finance where venture capital ran away, while also commissioning high-level innovative private sector activity that would not have happened without public policy goals backing a strategy and vision” (Mazzucato 2015: 79). Common practices to encourage innovation also include government subsidies and government procurements. Generally speaking, this type of industrial policy targets only frontier technologies. The state is not normally involved in the commercialisation of these technologies.

The Market-Facilitating State

The main goal of the market-facilitating state is to attract inflows of foreign direct investments in order to promote economic growth and participate in the international division of labour. Drawing upon the Chinese experience in creating the Special Economic Zones (SEZs), new structural economics considers factor endowment the most important criterion by which an economic entity chooses a path for economic growth. It maintains that an entity can enjoy comparative advantage in international trade only when it chooses to invest in industries permitted by its factor endowments in a given developmental stage, often measured by its capital-labour ratio. According to its reasoning, factor endowments do not directly represent comparative advantage because a lack of infrastructure and high transaction costs are often the primary barriers that prevent an economic entity from transforming its factor endowments into comparative advantage. In other words, comparative advantage will never be reached if one simply waits for market forces to work. Thus, the state must step in, concentrating its limited resources to actively remove these barriers. “A capable state is the precondition for an effective market, while building an effective market is all that a capable state should do” (Lin 2013; Lin 2017). The policy practised by the market-facilitating state in China until the beginning of the 21st century, with a few exceptions, was not really industrial policy but horizontal pro-growth policy as it was driven not by technological concerns, but by a motivation to promote economic growth in the most efficient way possible.

The Competitive-Advantage-Building State

After China joined the World Trade Organisation (WTO) in 2001, and especially once the Chinese economy began to promote industrial upgrading and innovation driven by the pressures of currency value appreciation, the state started to shift its focus from comparative advantage towards competitive advantage. Competitive advantage can be characterised by a hexagon diagram, the components of which include: strengthening factor supply by upgrading the qualities and increasing the types of factor endowments; building infrastructure in order to reduce the cost of business operations; improving institutional environments to reduce companies’ transaction costs; expanding market demand in an effort to create an economy of scale; developing industrial clusters for deepening the division of labour and advancing specialisation; and encouraging sector competition aiming at promoting productivity and innovation. The state treats the development of these six areas as the main goal of its industrial policy (Gao and Zhu 2020).

It may look like this hexagon diagram simply adds two components advocated by new structural economics—building infrastructure and reducing transaction costs—to Porter’s diamond diagram of competitive advantage (Porter 1990). However, the hexagon diagram has altered the conceptualisations of comparative/competitive advantage in two important ways. First, it redefines the concept of factor endowment. Porter distinguishes between basic factors and advanced factors, with the former referring to the natural endowment emphasised by classical trade theory and the latter referring to those factors acquired through human effort (Porter 1990). New structural economics treats basic factors as the foundation of its reasoning, contending that an economic entity should develop only those industries permitted by its present capital-labour ratio. In contrast, we focus on the advanced factors discussed by Porter and place more emphasis on the important role of human agency in creating and enhancing factor supplies. Second, the hexagon brings the state back into the model by proposing a causal relationship between state industrial policy and competitive advantage. Although Porter acknowledges that the state is relevant to each facet of his diamond diagram, he fails to connect them with the state in his conceptualisation. In contrast, we highlight the impacts of state industrial policy on the hexagon diagram of competitive advantage and treat this policy as the determining factor that shapes the development of competitive advantage.

The competitive-advantage-building state is not a unified national model. Even among local governments in China, there is a large range of variations in practice. However, the common features we discuss above are distinctively observable in the most competitive industries of the Chinese economy, as well as in most dynamic cities in the country. Instead of leaving the fate of the digital economy to market forces, the competitive-advantage-building state actively intervenes. Nevertheless, it does not simply pick the winners, as some critics have suggested, nor does it let the state itself replace private companies. Rather, as its label suggests, the competitive-advantage-building state considers its mission to be the creation of a favourable environment at the macro and meso levels in which companies grow competitive via their own entrepreneurship and market strategies.

Data as Factor Endowment

One of the most profound industrial changes since the 1990s is that data have become an important factor endowment. As Srnicek points out, “just like oil, data are a material to be extracted, refined, and used in a variety of ways. The more data one has, the more uses one can make of them” (2017: 40). Data have profound economic implications: “they educate and give competitive advantage to algorithms; they enable the coordination and outsourcing of workers, they allow for the optimisation and flexibility of productive processes; they make possible the transformation of low-margin goods into high-margin services; and data analysis is itself generative of data, in a virtuous cycle” (Srnicek 2017: 41–2).

The development of infrastructure has bestowed China with a special competitive advantage in international competition. Internet, fibre optics, smart phones and satellites provide the most important infrastructure for data production. China is advanced in all these fields. As Table 10.1 shows, by 2018, fibre optic broadband accounted for 82 per cent of China’s telecom network: the country had 600 million interfaces and 260 million users; the percentage of 4G users in the total population was more than double the global average; China had 760 million cell-phone users, the most in the world; and China, the US and Russia were the only three countries in the world with an operating global position system (Wang Jiwu 2018). In addition, China had 202 supercomputers, 43.8 per cent of the world’s total, while the United States owned 116, or 23.2 per cent (Zhongguo cunchu wang 2019).

Table 10.1: Digital Infrastructure in China

Digital infrastructure | China | Global | |

Internet | |||

Fibre optic broadband households (100 million) | 2.6 | – | |

User penetration rate (%) | 82 | 48 | |

Mobile network users | 7.6 | 30.7 | |

Global Navigation Satellite System | COMPASS | GPS(USA) GALILEO(EUR) GLONASS(RUS) | |

TOP 500 Supercomputers | 202 | accounting for 43.8% of global top 500 supercomputers | |

Sources: CAICT 2017, Wang Jiwu 2018, Zhongguo cunchu wang 2019.

In 2010, the Chinese government designated both Hangzhou and Shenzhen as trial cities for cloud computing, along with Beijing, Shanghai and Wuxi (National Development and Reform Commission, Ministry of Science and Technology 2010). Alibaba and Tencent, the two biggest platform companies in China, became the major players in developing both cities’ cloud computing industries.

As a leading platform of e-commerce, Alibaba had already collected huge amounts of data from both buyers and sellers long before it built cloud computing capability. Different from Amazon and JD that both buy and sell merchandise, Alibaba does neither but instead provides only platforms where buyers and sellers meet for their transactions. Such platforms rely heavily upon digital eco-systems. Alibaba developed two indispensable infrastructures to support its e-commerce platforms: the payment system, Ali Pay and the logistic system, Cainiao. These infrastructures further extended Alibaba’s data collection to both consumer finance and logistics. Cainiao is not a delivery company; rather, it is a logistics platform where individual consumers meet logistics service providers. Because of this, Alibaba’s range of data collection reached the entire logistics industry.

Tencent started as an instant messaging tool. Its early business model saw income generated by serving as a portal, providing traffic to China Mobile and taking a share of the profits. After its cooperation with China Mobile ended in 2005, Tencent adopted an “online living” strategy (Huaerjie Jianwen 2019). In 2010, when 90 per cent of Tencent’s employees still worked on PC versions of products and services, Tencent had already copied and combined every successful app in the industry into a single one-stop platform to fulfil its customers’ needs through a variety of services. Even before WeChat was invented in 2011, Tencent had built multiple platforms such as QQ, QQ Space, QQ Gaming and Tencent Network. Early on, Tencent developed storage and sharing functions for its platforms with a variety of technical supports for these services (Wu Xiaobo 2017).

The Premise of the Competitive-Advantage-Building State

Producers and service providers compete with each other in market economies. When an economic entity gains extra demand as a result of the competitiveness of its products and services in non-home markets, it experiences accelerated capital accumulation, stimulating new investments, increased expendable income of its residents, improved government tax revenues and overall economic well-being for the economic entity as a whole. This in turn strengthens the legitimacy of the ruling party in the government.

However, the competitiveness of products and services does not come about in a vacuum and its development is affected by various structural and institutional conditions. Without state intervention, the hexagon diagram of competitive advantage might still evolve, sustained by market forces, but it would take a much longer time and face dire uncertainties. In the face of cross-entity competitive pressures, the competitive-advantage-building state must step in to help create structural and institutional conditions that can strengthen the competitiveness of the companies that operate within its territory. In terms of the scope of intervention, the competitive-advantage-building state does more than its intervention-state counterparts, including the developmental state, social protection state, entrepreneurial state and market-facilitating state. Nevertheless, it restricts its actions to helping companies create their own competitiveness, rather than becoming a player directly in the market.

Enhancing Factor Endowments

Developing the digital economy demands venture capital and skilled labour with a high level of specialisation in information technologies. The industrial policy practised by the competitive-advantage-building state in both Hangzhou and Shenzhen has focused on enhancing these factor endowments by luring venture capital to high-tech industries using government investment funds.

As Table 10.2 demonstrates, in Hangzhou, the government offers four types of financial aid to develop technology in the region: designated funds for specific projects, guaranteed loans, angel-stage investor funds and working capital loans.

Table 10.2: The Investment and Financing Services Provided by the Hangzhou Government

Type of investment and financing | ||

Hangzhou venture capital guidance fund | ||

Designated funds (number) | 47 | |

Fund amount (billion yuan) | 6.6 | |

Funds from the government (billion yuan) | 3.3 | |

Funds from the market (billion yuan) | 2.3 | |

Start ups’ share of invested programme (%) | 71 | |

Loan guarantee for medium-sized and small tech companies | ||

Companies serviced in recent 10 years (times) | 2000 | |

Accumulated amount of loan guarantee (billion yuan) | 7 | |

Dandelion angel investment guidance fund | ||

Angel-stage fund (number) | 34 | |

Fund amount (billion yuan) | 2.1 | |

Number of projects invested | 184 | |

Funds from the government (billion yuan) | 0.45 | |

Funds from the market (billion yuan) | 0.45 | |

Hangzhou share of invested programme (%) | 65 | |

Hangzhou share of investment amount (%) | 71 | |

Working capital loan for medium-sized and small tech companies | ||

Working capital loan amount (billion yuan) | 1.5 | |

Companies that serviced working capital loan | 185 | |

Source: Yearbook of Hangzhou Science and Technology 2017.

By 2016, Hangzhou had established 47 different designated funds valued at 6.6 billion yuan, 3.3 billion of which came from the government and 2.3 billion from private investors. Of the projects that use these investments, two-thirds were conducted by local companies. 71 per cent of the investments went to start ups (Yang Zuojun 2017: 65).

In 2006, Hangzhou began offering guaranteed loans to support venture capital investment in technology. In the ten years from 2006 to 2016, Hangzhou’s guaranteed loan programme financed more than 2,000 projects at a total of 7 billion yuan. Since 2012 the Hangzhou government has financed more than 5 billion yuan in loans to small tech companies to fund over 800 different projects. Specifically to help entrepreneurial college students, Hangzhou established the Risk Pool Fund worth 35 million yuan with 4 million provided by the government, 1 million by a group of ten advisors, and the remainder from various banks (Yang Zuojun 2017: 65).

By 2016, Hangzhou had established 34 joint angel-stage funds totalling 2.1 billion yuan in available money provided by the government and private capital investors. These funds had financed 184 projects with 453 million yuan from the government and 445 million yuan from private capital. Of these projects, 65 per cent were conducted by local companies accounting for 71 per cent of the invested capital (Yang Zuojun 2017: 65).

In order to support small tech companies Hangzhou has also provided working capital loans. In 2016, 100 million yuan of such loans financed 185 projects of small tech companies and the loan amount totalled 1.5 billion yuan. The average amount for each project was 8.12 million yuan, with an average length of loan borrowing of 10 days. Since 2012, when Hangzhou started this programme, it financed more than 800 projects with 5 billion yuan. 95 per cent of these projects came from small tech companies (Yang Zuojun 2017: 64–5).

Shenzhen, according to Table 10.3, established three government investment organs to finance innovation in high-tech industries. The Shenzhen Innovation Investment Group, established in 1999, has been ranked number one in China’s venture capital industry over multiple years. It provides up to 30 per cent of the total investment capital for a fund, and the remaining 70–80 per cent must be raised from the market (Huang Ting 2018). A state’s adopted industrial policy will be unlikely to succeed if it is poorly received by the market because private venture capital is not willing to gamble on risky projects. The state’s 30 per cent financing alone is not enough to directly support innovation, so the state depends on private capital. At the same time, by offering 30 per cent of the capital, the state signals to the market that it supports the investment which is often enough to help convince venture capitalists to join in the investment.

Table 10.3: The Investment and Financing Services Provided by the Shenzhen Government

Type of investment and financing | ||

Shenzhen Venture Capital guidance fund | ||

Fund scale (billion yuan) | 100 | |

Number of projects invested | 681 | |

Investment amount (billion yuan) | 42.8 | |

Joint investment of social capital (billion yuan) | 357 | |

Shenzhen share of investment amount (%) | 42.4 | |

Angel investment guidance fund amount (billion yuan) | 5 | |

Source: Shenzhenshi caizheng weiyuanhui, 2018.

The Shenzhen Investment Holding Company is 100 per cent owned by the city’s State-Owned Assets Administrative Commission. It came into being as a result of the merger of three state-owned assets management companies in 2004. It has a majority share in more than 60 companies and minority shares in more than 20 companies. At the end of 2016, its assets totalled 53 million yuan (Nanfang Dushibao 2017).

The Shenzhen Angel Seed Fund was established in 2018. It provides 40 per cent of the total capital for a given project. In November 2018, the fund signed contracts with 8 private venture capital companies to provide 1.96 billion yuan on top of the 4.9 billion yuan these companies had pledged. Although the state shares the risks associated with investment, it does not share in the profits, except to recover its original investment amount (Liu Quan 2018). This practice is identical to that of the entrepreneurial state.

Human capital is another factor endowment that these two local governments have enhanced. Hangzhou began to adopt a human capital policy in 2004 (Hangzhou Municipal Communist Party Committee and Hangzhou Municipal People’s Government 2004). Information technology was one of the areas of expertise listed along with journalism, culture, finance, tourism, trade, management and law. Early on, Hangzhou tried to attract both those who held PhD or Master’s degrees and those without degrees who had high level skills. The government put forward a special policy to attract highly skilled workers and promoted various vocational programmes.

According to a 2017 study by LinkedIn, Hangzhou is number four in the distribution of human capital among Chinese cities in the digital economy, accounting for 3.4 per cent of the national total of skilled workers, led only by Shanghai (16.6 per cent), Beijing (15.6 per cent) and Shenzhen (6.7 per cent) (China Digital Economy Talent Report: 7). By September 2019, Hangzhou had attracted 55,000 university graduates from overseas with various degrees, plus 30,000 foreigners. They established 2,754 companies with 41,700 patents. Thirty-one of these companies have issued their IPO. For nine years in a row, Hangzhou has been selected as “the most attractive Chinese city for foreign talents”. Since 2016, Hangzhou has been ranked number one in terms of inflow of talent, inflow of talent from overseas and inflow of talent in internet-related industries (Fu Lingbo 2019).

In 2008, the Guangdong provincial government started a programme called “Empty the cage, welcome new birds”. Shenzhen announced a first-of-its-kind policy to attract senior-level talent in high-tech industries. In 2011, the year it adopted a policy to promote cloud computing, it also announced the famous “Peacock Program”. By 2017, Shenzhen had successfully attracted 14 research teams, including 4,309 persons from overseas, with 35.7 per cent in artificial intelligence, 28.6 per cent in big data and the internet of things and 7.1 per cent in cloud computing (Shenzhen Technology and Innovation Commission 2018).

Shenzhen has also tried to attract young labour with higher education. In 2011–17, Shenzhen’s population with local registration increased from 3.1 million to 4.4 million, with an average age of 27 (Shenzhen Statistical Yearbook 2018). In 2017 alone, Shenzhen attracted 174,000 college graduates, 18,307 returnees with overseas degrees ranging from a Bachelor’s to PhD, 935 postdoctoral fellows, and 12 Chinese Academy of Sciences and Chinese Academy of Engineering fellows to work full-time in Shenzhen (Shenzhenshi Renli ziyuan he Shehui baozhang June 2018).

Building Infrastructure

Building infrastructure is a distinctive feature of the industrial policy adopted by the competitive-advantage-building state in China. In the digital economy era, infrastructure involves platforms of public services and hardware infrastructure that support the development of the internet of things, big data, cloud computing and artificial intelligence.

In 2016, Hangzhou opened the Qiantang Big Data Trading Center, the first trading platform for industrial data in China. Its aim is to build an effective, convenient, and open-source database for the collection, trading and service of big data that can be provided to government agencies, industrial corporations and individual users. Its services include industrial data evaluation, initial data treatment, algorithms and modelling and data application products (Hangzhou zhengfuwang 2016). The Shenzhen government has also built platforms for public services, involving the development of commonly-shared technologies, quality certification, measurement and testing, data mining, information services, shared equipment, management services and the training of skilled labour. It established the Shenzhen Industrial Design Cloud Service Platform at the National Supercomputing Center of Shenzhen in 2015.

Opening government data to the public serves as an infrastructural support for the development of cloud computing. These data help companies improve their technologies. Open data mean that companies can dispatch resources and clean data via cloud networks, improve their capabilities in business analytics, increase the value of their apps and enhance artificial intelligence training. In September 2015, the Zhejiang Provincial government publicly announced its Open Data Platform. The data came from 68 government agencies and involved eight major areas, including economy, environment and natural resources, urban development, transportation, education/science/technology, culture and leisure, civil service and other organisations (Hangzhouwang 2015). By 2018, Shenzhen had made data available to the public in 14 areas, including transportation and traffic, finance and money, culture and leisure, education and science, and ecological resources. These data involved 79 million items and 1,094 datasets from 42 government agencies (Shenzhen Shang Bao 2018).

Reducing Transaction Costs

The development of the digital economy necessitates collaboration between basic research, R&D, intellectual property right transactions and commercialisation. Improving institutional environments serves to reduce transaction costs among different players.

Hangzhou has focused on protecting intellectual property rights. Zhejiang province is a leader in intellectual property rights protection in China. In 2011–16, Zhejiang courts accepted 76,000 intellectual property rights cases, which accounted for 51.3 per cent of the total cases in the Yangzi River Delta region. The courts settled 8,364 cases that involved patents, which accounted for one-sixth of such cases settled by the Chinese courts. These cases involved 1,759 high tech/new tech companies and 720 million yuan (Pengpai Xinwen 2017). In September 2017, Hangzhou, upon the approval of China’s Supreme Court, established its own Intellectual Property Rights Court. By October 2018, this court had settled 1,246 cases including 996 cases of IP rights violations and 250 cases of fake patents (Hangzhoushi Kexue Jishu Ju 2019).

Shenzhen lacks higher education institutions, and its R&D capacity has been concentrated in private companies. Its government has encouraged collaborations between academic institutions that conduct basic research and private companies that try to commercialise the outcomes of basic research. To accomplish this, the Shenzhen government made a special arrangement: when private companies build new labs jointly with universities or research institutions or upgrade old ones, the government invests up to 40 per cent of the total cost, up to five million yuan (Shenzhen Municipal Government 2011). By 2017, more than 20 labs, engineering centres, and technology centres had been established for the internet of things and 6 labs and centres had been established for artificial intelligence. In 2018, 10 such labs and centres were built specifically for big data (Shenzhen Technology and Innovation Commission 2018).

The government also started so-called “double-chain integration” projects. The two “chains” involve the chain of innovation and the chain of industry. Double-chain integration projects are driven by strong demand in the market which in turn intensifies the focuses on the basic research needed for frontier technologies, R&D for commonly shared technology and the demonstration model for commercialisation. Shenzhen pushed connections between industry and universities or research institutions by encouraging joint R&D. It provided 15 million yuan, per project, per year, for up to three years, and up to 30 per cent of the total investments (Shenzhen Jingxin Ju 2017).

Creating Market Demand

In the digital economy, size matters. The bigger the e-commerce is, the more data, and the more data, the bigger the cloud computing industry. An important role played by the competitive-advantage-building state is to create demands for new products and services for these new industries. In China, more than 300 regional-level cities have invested more than 600 billion yuan in cloud computing out of more than 3 trillion yuan pledged by these cities (Chen Jing 2018).

Hangzhou has focused on increasing application scenes, promoting government procurements and encouraging companies’ transition to cloud computing. Hangzhou requested the district and county governments within its jurisdiction to purchase cloud computing services in smart transportation, smart city-rural administration, smart public security and forest-ecology security monitoring.

Encouraging private companies to shift towards cloud-based IT infrastructure has been a major focus for Hangzhou. Hangzhou announced a three-year plan in 2018. It urged government agencies to provide guidance to private companies according to the characteristics of their industries. For example, agricultural companies should focus on building a platform for cloud computing that provides applications to data-source integration, product management, supply chain management, marketing and safety tracing; companies in the manufacturing industry should develop cloud applications that help R&D, production, supply chain management and marketing; and companies in the service sector should develop cloud platforms that help marketing management, sales channels, customer service and business operations. In 2017, Hangzhou pushed more than 41,500 companies to transition to cloud computing (Zhejiangsheng Jingxin Ting 2018).

Shenzhen has focused on the smart city programme, centred around urban management and digitalisation of public administration. The former involves water, electricity, gas, sewage, telecommunications, the subway and underground pipelines (Shenzhenshi renmin zhengfu bangongting 2013). The city built a comprehensive database and unified platform, providing basic information services that were needed for the approval process of civil engineering projects and underground pipeline network management. It also set data collection standards, clarified database structure and content requirements and outlined data renewal and sharing mechanisms.

The centralisation and digitalisation of public administration data have created a huge demand for cloud computing. Shenzhen pushed the transition of the government’s IT system from self-maintained to cloud, and the shift of government databases from business recording to business analytics. Between 2011 and 2018, the Shenzhen government had 175 data digitalisation projects involving 92 agencies at a cost of 15.6 billion yuan (Shenzhen Audit Bureau 2018). These projects involved information infrastructure hardware, software development, data collection, data cleaning, analytics, data application and solution design. In public services, these projects covered bureaux in charge of finances, economy and information, police, health, education, social welfare, transportation and construction.

Promoting Industrial Clusters

The spatial concentration of value chain, or industrial clusters, has been a distinctive Chinese practice over the past four decades and constitutes the basis for Chinese companies’ competitiveness. In order to promote the development of the cloud computing industry, Hangzhou has focused on building ecosystems for platforms. The cloud computing industry, just like other industries in the digital economy, is characterised by numerous small companies that form varieties of ecosystems. In its 2013–15 E-commerce Plan, Hangzhou invested 313 million yuan to strengthen its e-commerce platform and related value chains. It also invested 4.8 billion yuan for 44 platforms that provided public services (Hangzhoushi Jingxin Ju 2013). Hangzhou partnered with Alibaba to create “the Yunxi Village” in 2013, the first industrial cluster in China specialising in cloud computing and big data (Fu M. 2017). By 2018, it had gathered 645 companies related to cloud computing, generating one billion yuan in annual tax revenue. The major goal of this cluster was to encourage collaboration among innovative companies in regard to business conceptualisation, production, data analytics and service supplies in support of cloud computing end users (Zhejiang Zaixian 2015).

In Shenzhen, recruiting high-tech teams, rather than individual experts, became a major strategy for enhancing human capital. Between 2011 and 2017, through its Peacock Program, Shenzhen recruited senior research teams or start-up teams in robotics and smart information technology, data management, chips, 3D sensors, natural interaction between humans and machines, visual recognition and machine learning, robotic de-escalators, and the internet of things based on 5G. Huaao Data, a company that specialised in data cleaning, had applied for 113 patents, published 82 articles in top international journals and participated in the making of 16 industrial standards, five of which became national standards (Nanfang dushibao 2016). Yunxin Yihao, a maker of chips used in cloud technologies, provides comprehensive big data products and solutions. It expanded the cloud computing industry’s value chain and stimulated related industries’ development. It was the fourth company in Guangdong Province, after Huawei, Tencent and ZTE, to receive big data certification from the Ministry of Industry and Information (Nanfang Ribao 2017).

Encouraging Competition

Fair competition between government agencies or state-owned enterprises and private companies has been a major issue in China. Hangzhou established a fair competition review system in 2017. It required that any regulation, administrative order, or policy adopted by government agencies or organisations that perform public functions must receive a fair competition review when they involve market access, industrial development, foreign direct investment, bidding, government procurement, business regulation or industrial standards. More importantly, it has made government agencies’ performance in delivering these promises part of the evaluation system of government officials (Hangzhoushi Kexue Jishu Ju 2018).

Both cities have adopted universal criteria for the initial rounds of distribution of investment funds distribution or subsidies. So long as a company qualifies, it can receive the money. However, in order to receive funding or subsidies in subsequent rounds, a company has to meet a different set of criteria. Although the criteria for later rounds are still universal, the bar is higher with a company having to survive market competition to qualify.

The Political Economy of the Competitive-Advantage-

Building State

The above analyses show that the development of both Hangzhou and Shenzhen into two cloud computing powerhouses has been supported by the industrial policy adopted by the competitive-advantage-building state. However, industrial policy alone cannot explain the different outcomes. Table 10.4 shows that in the Infrastructure as a Service (IaaS) sector of the cloud computing industry, Alibaba is number one, accounting for 45.5 per cent of the market, while Tencent is a distant number two with only a 10.3 per cent market share. In the Platform as a Service (PaaS) sector of the same industry, Alibaba is also number one, accounting for 27.3 per cent of the Chinese market while Tencent does not even appear in the top five (Yiou Zhiku 2019b). Why is Alibaba’s market share in China more than four times larger than Tencent’s?

Table 10.4: The Top Five Companies in the Chinese Public Cloud Computing Market

IaaS (market share %) | PaaS (market share %) | ||

Alibaba Group | 45.5 | Alibaba Group | 27.3 |

Tencent | 10.3 | Oracle | 9.7 |

China Telecom | 7.6 | Amazon Web Services | 9.7 |

Kingsoft | 6.5 | Microsoft | 5.8 |

Amazon Web Services | 5.4 | IBM | 4.5 |

Others | 24.7 | Others | 43.0 |

Source: Yiou Zhiku 2019b: 26–7.

To answer this question, we need to examine the structural constraints on the competitive-advantage-building state: First, such a state is a product of the distribution of power in state-business relations. It tends to appear in places where private companies, either domestic or foreign, are predominant. Second, private companies’ preferences are crucial to the extent to which an industrial policy gets support, and their preferences are often derived from their business models. Third, the industrial policy of the competitive-advantage-building state is often affected by those leading private companies that have succeeded in breaking through from 0 to 1. Finally, the implementation of an industrial policy creates market dynamics that often incentivise those who had been reluctant to participate to change their minds.

The Power Distribution in State-Business Relations

Why has the competitive-advantage-building state emerged in Hangzhou and Shenzhen? Part of the answer lies in the structure of corporate ownership that indicates the power distribution in state-business relations.

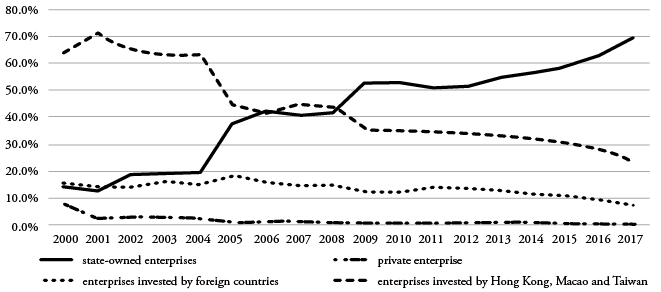

In both cities, private companies are predominant. Shenzhen started as a Special Economic Zone. As late as 2000, the number of foreign-invested companies, including those from Taiwan, Hong Kong and Macao, and the industrial outputs produced by these companies accounted for nearly 80 per cent of the city’s total. Between 2000 and 2017, as shown in Figure 10.1, a major shift took place: the number of domestic private companies increased from 15 per cent to nearly 70 per cent, while these domestic companies’ outputs grew to more than 50 per cent of the city’s total. In the same period, the number of foreign-invested companies declined by one-third, and the weight of companies from Taiwan, Hong Kong and Macao declined dramatically from more than 60 per cent to less than 20 per cent while their industrial outputs also declined significantly. The share of state-owned enterprises has been negligible in Shenzhen (Shenzhen Statistical Yearbook 2001–2018).

Figure 10.1: The Distribution of Ownership of Industrial Enterprises[1] in Shenzhen between 2000 and 2017

Source: Shenzhen Statistical Yearbook 2001–18.

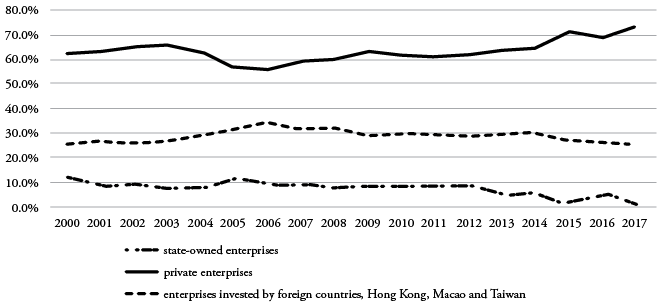

In contrast to Shenzhen, with its history of a high number of foreign-invested companies, domestic private companies have always been predominant in Hangzhou. Between 2000 and 2017, as shown in Figure 10.2, the number of investments in companies by foreign countries and by Taiwan, Hong Kong and Macao amounted to 17 per cent of companies on average annually, while their industrial output accounted for less than 30 per cent of the city’s total (Hangzhou Statistical Yearbook 2001–2018).

Figure 10.2: The Distribution of Ownership of Industrial Enterprises in Hangzhou between 2000 and 2017

Source: Hangzhou Statistical Yearbook 2001–18.

As opposed to Shenzhen where private companies’ production activities have been driven completely by international markets ever since the early 1980s, Hangzhou has been driven by domestic markets. In both cities, the elements and legacies of China’s planned economy had been weak, making it virtually impossible for the state to take a heavy-handed approach to practise industrial policy; the government had to find a way to implement its policy, such that it would work with the market.

Business Model and Preferences of the Private Sector

Why has Hangzhou taken the lead in cloud computing while Shenzhen has been left behind? The answer is that the industrial policies in each city have been heavily affected by the preferences of the leading companies in the industry, and those preferences were often derived from their business models.

At an IT summit in March 2010, the leaders of China’s big three platform companies, Baidu, Alibaba and Tencent, had a famous debate about cloud computing. Alibaba’s CEO Jack Ma was very optimistic, foreseeing cloud computing to be the future direction of information technology. In contrast, both Tencent’s CEO Pony Ma and Baidu’s CEO Robin Li were pessimistic: the former held that the era of cloud computing would not come for another hundred years, while the latter considered cloud computing as nothing more than a “new bottle of old wine”. These leaders’ positions on cloud computing are largely responsible for their companies’ relative positions in the industry today.

Alibaba’s eagerness to develop cloud computing was driven by the bottleneck in its IT infrastructure amid the rapid growth of its e-commerce business. Before 2008, Alibaba’s IT infrastructure relied heavily upon IOE, namely, IBM’s servers, Oracle’s database and EMC’s data storage. At the time, Alibaba’s business was growing by more than 30 per cent a year and its computing facilities ran at nearly full capacity every morning. An unexpected system breakdown became a lingering nightmare. Because IOE equipment was expensive, Alibaba could no longer bear the cost of upgrading its IT infrastructure. After several system breakdowns, Alibaba decided in 2008 that cloud computing was its only life-saving solution. So, even without government support, Alibaba started its R&D on cloud computing (Shi Zhong 2018).

Former deputy director of Microsoft Institute Asia and Ali Cloud CEO Wang Jian’s vision plus Alibaba CEO Jack Ma’s firm support played a crucial role in the development. The development process was quite bumpy. In more than three years, cloud computing was not well received within Alibaba. Subunits were not willing to try it, Wang was even called a swindler, and 80 per cent of the R&D team members quit because they had lost confidence in the project. Despite all this, Jack Ma never gave in. In fact, he proceeded to announce that Alibaba would invest one billion yuan per year for the next ten years to develop the Ali Cloud (Wei Wuji 2018). One impetus behind this effort was when, in 2009, Alibaba started to have an annual sales event on November 11th, China’s “Singles’ Day”. This holiday has since become the most important commercial day for Chinese consumers and businesses. Future November 11th holiday sales presented great challenges to Alibaba’s website because the flood of orders that pour into it each second could easily lead to a system breakdown, potentially costing the company millions. Cloud computing’s promise of a solution firmed up Jack Ma’s support for developing Ali Cloud.

In contrast, Tencent’s journey towards cloud computing was driven by a number of circumstantial events. In 2010, the same year in which Pony Ma presented his pessimistic view about cloud computing, Qihu 360, an internet security company, launched a big lawsuit against Tencent. Although Tencent won the lawsuit in court, public opinion about Tencent was decidedly negative. Its early model of copying every successful app earned Tencent the nickname “public enemy of all industries”. This forced Pony Ma to reflect (Wu Xiaobo 2017). In 2010, Tencent invented WeChat and it grew rapidly. WeChat’s popularity was further enhanced by a profound shift in China’s internet industry in 2012: the number of smart phone users surpassed the number of PC users.This marked the beginning of a new era in which social media would become dominant. As the digital economy became more complicated, it was no longer possible to develop everything in house. In addition, Tencent’s competitors, such as Baidu, Sina and Alibaba, all adopted an open door strategy. Under the pressure of competition, Tencent was forced to open its own platforms to outsiders allowing third party companies to use its platforms. Of course, Tencent still received a share of these companies’ profits by providing the gateway to the customer pool and basic infrastructural services (Liu Hongjun 2019).

Although Alibaba had the first-comer’s advantage, the different perceptions and adoption models of cloud computing determined the private companies’ and consequently these cities’ positions in the industry. However, some puzzles still remain: why was Shenzhen left behind even after it adopted an industrial policy to support cloud computing several years earlier than Hangzhou did? And why did Shenzhen set only a moderate goal for its cloud computing industry although it quickly responded to the industrial policy adopted by the central government?

Structural Constraints and the Agency of the State

The answer is that industrial policy is often shaped by private entrepreneurship and the effectiveness of an industrial policy is often affected by the willingness of private companies to follow the state’s guidance.

When the central government designated Hangzhou as one of the five trial cities for cloud computing in 2010, it provided Alibaba with 450 million yuan, while the company decided to invest 3 billion (Hangzhou Zhengfuwang 2012). Beginning in 2011, the Zhejiang provincial government provided some support for the development of the Ali Cloud but the amount of money was small. Up until 2014, Hangzhou’s municipal government had essentially been taking a wait-and-see position and did not adopt a specific policy to support cloud computing.

Even by mid-2014, Hangzhou was still uncertain about the future of its economy. Before that time, Hangzhou had primarily relied on low tech, high energy consumption, cheap labour, traditional business models and small companies. This development strategy reached a bottleneck in 2012: Hangzhou ended its 21-year two-digit economic growth, recording growth of only 9 per cent, and in 2013, it dropped further to 8 per cent (Yu and Tang 2017). Although Hangzhou was one of the five trial cities designated for cloud computing and was specifically chosen by the central government to be the national centre of e-commerce, Hangzhou had never taken these designations seriously. Even after more than 190 Chinese cities launched their own smart-city programmes in 2014, Hangzhou still thought this phenomenon was merely a fad.

Ali Cloud CEO Wang Jian’s advice changed government officials’ minds. At a meeting in which government officials solicited advice on new industries to generate economic growth, Wang told them that Hangzhou could become China’s data centre. He proposed that the digital economy represented by big data, cloud computing, the internet of things, the mobile internet and smart manufacturing could be the future direction for Hangzhou’s economy (Yu and Tang 2017). Wang gave this advice with great confidence: by mid-2014 Ali Cloud had proven a big success. When the Ali Cloud was tested for the first time during the largest shopping day of the year, Singles’ Day, 11 November 2012, it was able to survive a million simultaneous orders. By the following year, 11 November 2013, Alibaba’s cloud computing involved more than 5,000 computers operating in a network with its cloud processing 80 per cent of 35 billion orders in a single day (Yang Xiaohe 2018).

Once the government was convinced by Wang’s advice, it proposed an ambitious master plan: Hangzhou would become a major national centre for designing and planning cloud computing, building platforms for cloud computing and providing operation-maintenance services. It treated the development of the digital economy as its “number one priority” (Zhejiang Zaixian 2014). Cloud computing and big data, together with e-commerce, the internet of things, logistics, internet finance and digital content were considered a cluster of industries whose interactions would exert a positive impact on each other (Hangzhou Municipal Communist Party Committee and Hangzhou Municipal People’s Government 2014).

Since 2014, Hangzhou has concentrated its resources in the digital economy. It even substantially reorganised its internal division of labour by establishing the Bureau of Cloud Computing and Big Data within its Economy and Information Commission, the first such bureau in the country. It has also made two three-year development plans for e-commerce, 2013–15 and 2015–17 (Hangzhoushi Shangwu Weiyuanhui 2015). In 2018, Hangzhou announced the next stage of development for cloud computing which will bring artificial intelligence to the centre of its future industrial upgrades (Hangzhoushi Fazhan he Gaige Weiyuanhui 2018).

For its part, Shenzhen responded to the central government’s policy quickly. Only one week after it was designated one of the five trial cities for cloud computing in 2010, Shenzhen announced a cloud computing policy. It proposed further cloud computing policies in 2011 that included various measures to support the development of the industry. Nevertheless, the goals it set for itself were rather moderate: Shenzhen would become “a center of cloud computing in South China”. This lack of ambition was partly due to the fact that once a goal had been set, the performance of the local government might be evaluated accordingly. Given that the major local players, Tencent and Huawei, were less enthusiastic to embrace cloud computing technology, it was understandable that Shenzhen’s government was less ambitious.

Because Tencent was the biggest platform company in China, and third-party companies operating through the Tencent Cloud could gain access to all its platforms simultaneously, one would think that the Tencent Cloud should have surpassed Ali Cloud quickly. However, the problem was that even after Tencent started its cloud computing programme, it was not serious about it until 2017. Pony Ma rejected the programme director’s proposal to expand cloud computing into Tencent’s major business. Within Tencent, the cloud was merely a subunit of its Social Network Group, languishing in a situation in which “no external client use[d] it while no internal unit like[d] it”. Whereas Jack Ma of Alibaba forced his company’s subdivisions to use Ali Cloud, the Tencent Cloud did not enjoy that kind of internal support. Tencent did not have the gene of To-B business because it had been a To-C company. In 2018, the Tencent Cloud suffered from major accidents resulting in the loss of client data and the disruption of cloud functions. Only after Tencent’s profits declined by 35 per cent in the fourth quarter of the 2018 fiscal year did the company finally begin to take cloud computing seriously, after which the Tencent Cloud was upgraded to the Cloud and Smart Industry Group (AI Caijingshe 2019).

Huawei, another giant of cloud computing in Shenzhen, was in a similar situation. Huawei started its cloud computing programme in 2010. However, it took a strategy of “announcing the plan but not working hard on it”. Unlike other internet platform companies, cloud computing had the potential to directly hurt Huawei’s interests. According to its internal calculations, Huawei stood to make five times more profits when clients performed calculations on Huawei’s servers than it would make if those clients performed the same calculations in the cloud. It was only in 2016, after Alibaba and Tencent took away nearly 60 per cent of market share in the cloud computing industry, that Huawei finally made the decision to catch up to the competition (AI Caijingshe 2019).

The agency of Shenzhen’s government in implementing industrial policy for cloud computing was structurally constrained by the reluctance of two leading companies in the field. In addition, Shenzhen had been a centre of computer hardware without enough software engineers. Government officials could not do much when the private sector was not enthusiastic. At the same time, Shenzhen did not worry too much about its economic fortunes for two reasons: First, although Tencent is a major company in Shenzhen, the city has plenty of peers, such that Tencent is only one big company among many. Second, cloud computing is only one of several important industries in the city. Even as Huawei failed to actively participate in developing cloud computing, its telecom equipment and cell-phone businesses still provided the city with enormous tax revenues. So, Shenzhen did not mind if Huawei was not serious or took its time in developing its cloud computing capability.

Concluding Remarks

This study demonstrates the distinctive characteristics of the industrial policy practised by the competitive-advantage-building state in two Chinese cities. At the same time, it also shows that such a state draws upon various practices of other types of industrial policy. It shares the focuses of the developmental state in Japan, such as industrial targeting and promoting exports, but is more open to inflows of foreign capital and employs more policy tools to support private companies. When the state developed funding mechanisms to support the development of the cloud computing industry, for example, it went beyond the traditional government subsidies by creating government investment funds and also supporting private venture capital. By bearing the risks of investment in frontier technologies and by creating market demand through government procurement, the competitive-advantage-building state has also become more similar to that of the entrepreneurial state in the United States. Such a state encourages industrial rivalry in the digital economy and shows no mercy to those that fall short in competition. This is in a sharp contrast to the social protection state. Although it shares some practices of the market-facilitating state such as building infrastructure and reducing transaction costs, it is never satisfied by merely creating an effective market and always aims at helping companies that operate within its territory become more competitive. More importantly, the competitive-advantage-building state actively strengthens the factor supplies by both encouraging the development of venture capital and recruiting tech talent globally, transcending the practice of simply using the capital-labour ratio to decide which industries to target, as the market-facilitating state does.

For all other types of state intervention, industrial policy is often treated as the independent variable, which is used to explain the outcome. In contrast, our analysis extends a political economy investigation of industrial policy by turning the competitive-advantage-building state into an intervening variable. By doing so, our model reveals the impacts of both corporate ownership structure and private sector business models on state industrial policy. It demonstrates both the human agency that plays such an important role in practising state industrial policy, and the various constraints imposed by various structural conditions upon such agency.

Chinese industrial policy has often been portrayed as anti-competitive in both domestic and international debates. This may be true in cities that have relatively more state-owned enterprises in sunset industries in relation to which government policies are more similar to those practised by a social protection state. However, this is not true at the centre of China’s digital economy. The reason, as this study shows, is that the dominance of private companies in the ownership structure affects the power distribution in state-business relations. In high-tech industries, it is difficult both for the state to support a monopoly of state-owned enterprises, and for private companies to build monopoly positions amid fierce competition.

Contrary to the conventional image that the state practises industrial policy in a top-down fashion, the industrial policies of Shenzhen and Hangzhou municipal governments towards high-tech industries are often affected by private companies because the giant private companies themselves take the lead in innovation and carry out the breakthrough from 0 to 1. As Ali Cloud and Hangzhou’s industrial policy demonstrate, private companies’ vision and knowledge often become the blueprint of state industrial policy. At the same time, Shenzhen’s experience with Tencent and Huawei in cloud computing shows that the state cannot achieve its industrial policy goals when the leading private companies are not enthusiastic about them.

Note

[1] Industrial enterprises over levels refer to the industrial enterprises whose main business revenue reached the designated size, 5,000,000 yuan before 2010 and 20,000,000 yuan from 2010 to 2019.

References

AI Caijingshe [AI Finance]. 2019. Zhongguo yunjisuan de shinian nixi [The Return of China’s Cloud Computing]. Available at https://tech.sina.com.cn/roll/2019-10-04/doc-iicezzrr0013819.shtml [accessed 23 Nov. 2020].

Alibaba. 2019. Yin keiji, er yunxi [Because of Science and Technology, Here Comes Yunxi]. Available at https://yunqi.youku.com/ [accessed 23 Nov. 2020].

Alibaba Group. 2018. Alibaba jituan gongbu 2018nian 3yuedizhi jidu ji cainian yeji [Alibaba Group Announces Quarterly and Fiscal Year Results for the End of March 2018]. Available at https://www.alibabagroup.com/cn/news/article?news=p180504 [accessed 23 Nov. 2020].

Chen Jing. 2018. Zhihui chengshi leiji guihua touzi da 3wanyi, shuju jiazhi ying zai shenwa [The cumulative planning investment of smart cities reaches 3 trillion, the value of data should be further digging]. Zhongguo Jingjiwang. Available at http://www.ce.cn/cysc/tech/gd2012/201810/10/t20181010_30470624.shtml [accessed 23 Nov. 2020].

Chen Qingtai. 2016. Zhongguo chanye zhengce diwei zhi gao qiansuoweiyou, yi cheng zhuanxing zhangai [China’s industrial policy status is unprecedented, and it has become a barrier to transformation]. Xinlang Caijing. Available at http://finance.sina.com.cn/hy/hyjz/2016-11-27/doc-ifxyawmm3527483.shtml [accessed 23 Nov. 2020].

China Digital Economy Talent Report. 2017. LinkedIn Economic Graph Team. (in Chinese). Available at https://economicgraph.linkedin.com/research/china-digital-economy-talent-report [accessed 22 Feb. 2021].

Fu Lingbo. 2019. Hangzhou jiakuai gouzhu rencai gaodi [Hangzhou accelerates the construction of an international talent pool]. Hangzhou Daily. Available at https://hzdaily.hangzhou.com.cn/hzrb/2019/09/26/article_detail_1_20190926A259.html [accessed 23 Nov. 2020].

Fu M. 2017. “Yunxi xiaozhen shi zenyang liancheng de?” [How Did Yunxi Village Develop?]. Taimeiti. Available at http://www.sohu.com/a/205834637_116132 [accessed 23 Nov. 2020].

Gao Bai. 1997. Economic Ideology and Japanese Industrial Policy: Developmentalism from 1931 to 1965. New York: Cambridge University Press.

________. 2001. Japan’s Economic Dilemma: The Institutional Origins of Prosperity and Stagnation. New York: Cambridge University Press.

Gao Bai and Zhu L. 2020. “Cong ‘shijie gongchang’ dao gongye hulianwang qiangguo: dazao zhineng zhizao shidai de jingzheng youshi” [From “the World Factory” to A Strong Nation of the Industrial Internet of Things: Building Competitive Advantage in the Era of Smart Manufacturing]. Gaige 315, 5: 429–42.

Gartner. 2019. Market Share Analysis: IaaS and IUS, Worldwide, 2018. Available at https://www.gartner.com/en/documents/3947169/market-share-analysis-iaas-and-ius-worldwide-2018 [accessed 23 Nov. 2020].

Guanyan Tianxia. 2019. “2019nian zhongguo yunjisuan hangye shichang guimo kuaisu zengzhang” [The Size of the Cloud Computing Industry in China Grow Rapidly in 2019]. Zhongguo Baogaowang. Available at http://free.chinabaogao.com/it/201908/0Q43I042019.html [accessed 23 Nov. 2020].

Hangzhou Municipal Communist Party Committee and Hangzhou Municipal People’s Government. 2004. Guanyu dali shishi rencai qiangshi zhanlve de jueding [Decision on Vigorously Implementing the Strategy of Strengthening City with Talents]. Available at http://www.hangzhou.gov.cn/art/2004/4/21/art_809119_2306.html [accessed 23 Nov. 2020].

________. 2014. Guanyu jiakuai fazhan xinxi jingji de ruogan yijian [Several Opinions on Accelerating the Development of Information Economy].

Hangzhou Statistical Yearbook 2001–2018. Beijing: China Statistics Press.

Hangzhou zhengfuwang. 2012. Dishiwujie Hangzhou guonei jingji hezuo qiatanhui [15th Hangzhou Domestic Economic Cooperation Fair]. Available at http://www.hangzhou.gov.cn/art/2012/10/24/art_1003069_1332.html [accessed 23 Nov. 2020].

________. 2016. Qiantang dashuju jiaoyi zhongxin shangxian [Qiantang Big Data Trading Centre is online]. Available at http://www.hangzhou.gov.cn/art/2016/6/1/art_812262_724088.html [accessed 23 Nov. 2020].

Hangzhoushi Fazhan he Gaige Weiyuanhui [Hangzhou Development and Reform Committee]. 2018. Guanyu yinfa Hangzhou chengshi shuju danao guihua de tongzhi [Notice on Printing and Distributing the Planning of Hangzhou City’s Data and Brain). http://www.hangzhou.gov.cn/art/2018/5/15/art_1256296_18106029.html.

Hangzhoushi Jingxin Ju. 2013. Hangzhoushi dianzishangwu chuangxin fazhan sannian xingdong jihua (2013–2015) [Hangzhou E-commerce Innovation and Development Three-Year Action Plan (2013–2015)]. http://www.hangzhou.gov.cn/art/2013/4/3/art_1256297_7881522.html.

________. 2018. Hangzhoushi shenhua tuijin “Qiye shangyun” sannian xingdong jihua (2018–2020) [Hangzhou Deepens the Three-Year Action Plan for “Enterprise cloud migration” (2018–2020)]. Available at http://www.hangzhou.gov.cn/art/

2018/11/13/art_1256296_24510444.html [accessed 23 Nov. 2020].

Hangzhoushi Kexue Jishu Ju [Hangzhou Science and Technology Bureau]. 2018. 2018nian Hangzhoushi zhishichanquan zhifa weiquan gongzuo fangan [Hangzhou Intellectual Property Rights Enforcement Plan in 2018]. http://kj.hangzhou.gov.cn/index.aspx?newsId=48351&CatalogID=767&PageGuid=4A3B6524-953E-4CA2-A5C4-0DC81BDEF4CC.

________. 2019. 2018nian hangzhoushi zhishichanquan gongzuo zongjie [Hangzhou Summary of Intellectual Property Work of in 2018]. http://kj.hangzhou.gov.cn/index.aspx?newsId=49380&CatalogID=843&PageGuid=4A3B6524-953E-4CA2-A5C4-0DC81BDEF4CC.

Hangzhoushi Shangwu Weiyuanhui [Hangzhou Municipal Commission of Commerce]. 2015. Hangzhoushi jianshe guoji dianzishangwu zhongxin sannian xingdong jihua (2015-2017nian) [Three-year Plan of Action for Hangzhou to Build an International Electronic Commerce Centre]. http://sww.hangzhou.gov.cn/art/2015/9/15/art_1551501_29268679.html

Hangzhouwang. 2015. “9yue23ri Zhejiang zhengfu shuju kaifang pingtai shangxian, hangai bada lingyu 68 ge jiguo shuju” [On September 23 the Zhejiang Government put the Open Data Platform Online, which Involved Data from 68 Agencies in Eight Areas]. Hangzhou Bendibao http://hz.bendibao.com/news/

2015924/61007.shtm.

Huaerjie Jianwen [Wall Street]. 2019. “Fu pan tengxun 20nian” [Reviewing 20 years of Tencent]. Baijiahao. Available at https://baijiahao.baidu.com/s?id=1626907977547660824&wfr=spider&for=pc [accessed 23 Nov. 2020].

Huang Ting. 2018. “Shenchuangtou Sun Dongsheng: Yi erji guzhi daogua shi dagailü Shijian, shouyilü kending hui zoudi” [Shenzhen Capital Group Sun Dongsheng: A valuation inversion of the new issue and security markets is a high probability event, and the yield will definitely go down]. Lujiazui zazhi. Available at http://www.sohu.com/a/242882819_100191015 [accessed 23 Nov. 2020].

IDC [International Data Corporation]. 2019. 2019nian yijidu, zhongguo gongyouyun shichang renao kaiju [The First Quarter 2019, A Lively Start]. Available at https://www.idc.com/getdoc.jsp?containerId=prCHC45418919 [accessed 23 Nov. 2020].

Johnson, Chalmers A. 1982. MITI and the Japanese Miracle : The Growth of Industrial Policy, 1925-1975. Stanford CA: Stanford University Press.

Lin Yifu. 2013. “Zhenfu yu shichang de guanxi” [The Relationship between the Government and the Market]. Guojia Xingzheng Xueyuan Xuebao 6: 4–5.

________. “Lin Yifu: Zhengfu youwei shi shichang youxiao de qianti” [Lin Yifu: Active government is the premise of effective market]. Fenghuang Zhoukan. https://pit.ifeng.com/a/20170504/51043072_0.shtml.

Liu Hongjun. 2019. “Tengxun kaifang zhenxiang” [“The Truth about Tencent’s Opening”]. Huanqiu qiyejia. Available at http://www.gemag.com.cn/12/31479_1.html [accessed 3 Mar. 2021].

Liu Quan. 2018. “Jiemi Shenzhenshi tianshi mujijin” [Uncovering Shenzhen’s Angel Fund of Funds]. Touzijie. November 17th. Available at https://news.pedaily.cn/201811/437894.shtml [accessed 23 Nov. 2020].

Mazzucato, Mariana. 2015. The Entrepreneurial State: Debunking Public vs. Private Sector Myths. New York: Public Affairs.

Nanfang Dushibao. 2016. Huaao: Kaiken zhengfu shuju gudao [Huaao: Reclamation government data island]. Available at http://epaper.oeeee.com/epaper/A/html/2016-10/19/content_85846.htm [accessed 23 Nov. 2020].

________. 2017. Duibiao Singapore danmaxi konggu shentoukong 2020nian zichan zongguimo huochao 3wanyiyuan [Modelled on Singapore’s Temasek Holdings, Shenzhen Investment Holding Company’s Assets Will Reach 3 Trillion yuan in 2020]. http://www.sihc.com.cn/media_detail-3-61-1.html

Nanfang Ribao. 2017. Qianhaixinxi xie ‘Yunxin yihao’ luohu baoan [Qianhai Information Brings ‘Cloud Core One’ to Baoan]. Available at http://epaper.southcn.com/nfdaily/html/2017-03/28/content_7627599.htm [accessed 23 Nov. 2020].

National Development and Reform Commission and Ministry of Science and Technology. 2010. Guojia fazhan gaigewei Gongye he xinxi huabu guanyu zuohao yunjisuan fuwu chuangxin fazhan shidian shifan gongzuo de tongzhi [National Development and Reform Commission, Ministry of Industry and Information Technology Notice on Piloting and Demonstration of Cloud Computing Service Innovation and Development]. Available at http://www.gov.cn/zwgk/2010-10/25/content_1729805.htm [accessed 23 Nov. 2020].

Pengpai Xinwen [Breaking News]. 2017. Hangzhou, Ningbo zhishi chanquan ting guapai, ke kuaquyu guanli zhejiang sheng nei zhongda anjian [Hangzhou and Ningbo establish Intellectual Property Court, making the management of cross-regional major cases in the province possible]. Available at http://www.sohu.com/a/190601437_260616 [accessed 23 Nov. 2020].

Porter, Michael E. 1990. The Competitive Advantage of Nations. New York: The Free Press.

Shenzhen Audit Bureau. 2018. Shenzhenshi 2018niandu jixiao shenji gongzuo baogao [Report of Shenzhen 2018 Annual Performance Audit Work]. http://www.sz.gov.cn/sjj/qt/zyhy_1/201812/t20181225_14948279.htm.

Shenzhen Jingxin Ju. 2017. Zhanluexing xinxing he weilai chanye fazhan zhuanxiang zijin shenqing zhinan [Guide to applying for special funds for Strategic Emerging and Future Industries]. http://wap.sz.gov.cn/cn/xxgk/zfxxgj/tzgg/201706/t2017

0615_7126001.htm.

Shenzhen Municipal Government. 2011. Shenzhenshi Renmin Zhengfu guanyu yinfa xinyidai xinxijishu chanye zhenxing fazhan zhengce de tongzhi [Notice of the Shenzhen Municipal People’s Government on Printing and Distributing the Policy of Promoting the Development of Shenzhen’s New Generation Information Technology Industry]. Available at http://www.gov.cn/zhengce/2011-12/29/5043037/files/

82024f082d7145b79e2995652dab79bf.pdf [accessed 23 Nov. 2020].

Shenzhen Shang Bao. 2018. Shenzhen zhihui zhengwu zhuoyou chengxiao [Shenzhen Smart Government has achieved fruitful results]. Available at http://szsb.sznews.com/PC/content/201812/06/content_522878.html [accessed 23 Nov. 2020].

Shenzhen Technology and Innovation Commission. 2018. Shenzhen shi chuangxin zaiti mingdan [List of Shenzhen innovation institutions]. Available at http://stic.sz.gov.cn/kjfw/cxzt/szscxztmd/ [accessed 21 Nov. 2020].

Shenzhenshi caizheng weiyuanhui [Shenzhen Municipal Finance Committee]. 2018.

Shenzhenshi renli ziyuan he Shehui baozhang Ju [Shenzhen Municipality Human Resources and Social Security Bureau]. 2018. 2017nian Shenzhenshi renli ziyuan baozhang gongzuo zongjie he 2018nian gongzuo bushu [2017 Shenzhen Human Resources Guarantee Work Summary and 2018 Work Deployment]. http://www.sz.gov.cn/szrbj/xxgk/ghjh/jhjzj/201804/t20180428_11803536.htm.

Shenzhenshi renmin zhengfu bangongting [General Office of Shenzhen Municipal People’s Government]. 2013. Zhihui Shenzhen jianshe shishi fangan (2013-2015nian) [Smart Shenzhen Construction Implementation Plan (2013–2015)]. http://zwgk.gd.gov.cn/007543382/201310/t20131025_429290.html.

Shenzhenshi tongju ju. 2001-18. Shenzhen Statistical Yearbook. China Statistics Press.

Shi Zhong. 2018. “Aliyun de zhequn fengzi” [Alibaba Cloud’s Madmen]. Qianhei Keji. Available at https://yq.aliyun.com/articles/653511?spm=a2c4e.11153940

.0.0.2a60361awfKHCw [accessed 23 Nov. 2020].

Srnicek, Nick. 2017. Platform Capitalism. Cambridge UK: Polity.

Tilton, Mark. 1996. Restrained Trade: Cartels in Japan’s Basic Materials Industries. Ithaca: Cornell University Press.

Uriu, Robert. 1996. Troubled Industries: Confronting Economic Change in Japan. Ithaca: Cornell University Press.

Wang Jiwu 2018. “Wang Jiwu lun zhongmei zhizheng: renlei diwuci kejigeming yu chanye1geming” [Wang Jiwu on the China-U.S. Competition: The Ultimate Competition in the Fifth Scientific-Technological and Industrial Revolution]. Qidi Kungu. http://www.sohu.com/a/255488940_465915.

Wang W., Wei W. and Hua X. 2018. Tengxun 15nian shangye moshi bianqian [The Transformations of Tencent’s Business Models]. http://tech.ifeng.com/a/20140112

/45162067_0.shtml.

Wei Wuji. 2018. “Ta ceng ‘pian’ le Ma Yun 10yi, 10nian hou huanle 4500yi, cong pianzi dao dashi, ta shi ruhe Chenggong de?” [He “cheated” Jack Ma out of 1 billion yuan, and he paid back 450 billion yuan 10 years later. From cheater to master, how did he succeed?”]. Dianshang guancha wang. Available at http://finance.sina.com.cn/money/fund/fundzmt/2018-10-02/doc-ifxeuwws0479320.shtml [accessed 23 Nov. 2020].

Wu Jinglian. 2016. “Wu Jinglian: Chanye zhengce yizhi jingzheng, weifan gongping jingzheng yuanze” [Wu Jinglian: Industrial policy restrains competition, violates the principle of fair competition]. Xinlang Caijing. Available at http://finance.sina.com.cn/hy/hyjz/2016-11-27/doc-ifxyawmm3523035.shtml [accessed 23 Nov. 2020].

Wu Xiaobo. 2015. “Tengxun 17nian fazhanshi shang de 14ge guanjiandian” (The 14 Key Points in the 17 Year History of Tencent). Tengxuwang. 12 June. Available at https://tech.qq.com/a/20150612/019667.htm [accessed 23 Nov. 2020].

________. 2017. Tengxun zhuan [The History of Tencent]. Hangzhou: Zhejing Daxue Chubanshe.

Yang Xiaohe. 2018. “Zhongguo yunjisuan diedang shinian, huiwang aliyun kanke feitianlu” [Cloud Computing in China has been in Decline for Ten Years, looking back on Ali Cloud’s bumpy and winding Road]. Yi Ou. Available at https://www.iyiou.com/p/81080.html [accessed 23 Nov. 2020].

Yang Z. 2017. Yearbook of Hangzhou Science & Technology. Beijing: Zhonghua Shuju.

Yiou Zhiku. 2019a. Tengxun 2019 Q2 yeji gaozengzhang yanxu, tengxunyun zaici chengwei zengzhang yinqing [The High-Speed Growth of Tencent’s Performance has continued, Tencent Cloud became the Growth Engine Again]. Available at https://www.iyiou.com/p/109059.html [accessed 23 Nov. 2020].

________. 2019b. 2019nian zhonggou yunjisuan hangye fazhan yanjiu baogao [The 2019 Report on the Development of the Cloud Computing Industry in China]. Available at https://legacy.iyiou.com/intelligence/report615.html [accessed 23 Nov. 2020].

Yu J. and Dong J. 2019. “Woguo Shuzijingji gaimo da 31.3 yiyuan zhan GDP bizhong da 34.8%” [The Size of China’s Digital Economy reached 31.3 Trillion Yuan and Counts for 34.8% of GDP]. Xinhua News Agency. Available at http://www.cac.gov.cn/2019-05/06/c_1124458275.htm [accessed 23 Nov. 2020].

Yu Xina and Tang Junyao. 2017. “Hangzhou Jingxinwei Zhuren: Cong mimang dao jianding, women zenme zhaodao fazhan zhi lu” [Director of the Hangzhou Committee of Economic and Information Technology: From Confusion to Firmness, How can we Find the Way of Development?]. Zhejiang News. Available at https://zj.zjol.com.cn/news/606619.html [accessed 23 Nov. 2020].

Zhejiang Zaixian [Zhejiang Online]. 2014. Gong Zheng: Ju quanshi zhili jiandingbuyi zhuahao ‘yihao gongcheng’ [Gong Zheng: Take the strength of the whole city to firmly grasp the ‘No.1 Project’]. Available at http://hangzhou.zjol.com.cn/system/2014/08/23/020215484.shtml [accessed 23 Nov. 2020].

________. 2015. Hangzhou zheng xunsu chengwei Zhongguo hulianwang chuangye chuangxin gaodi [Hangzhou is Rapidly Becoming China’s Internet Entrepreneurial Innovation Highland]. Available at http://hangzhou.zjol.com.cn/system/2015/10/15/020872798.shtml [accessed 23 Nov. 2020].

Zhejiangsheng Jingxin Ting [Economy and Information Technology Department of Zhejiang]. 2018. Guanyu 2017 niandu ‘Qiye shangyun’ kaohe qingkuang de gongshi [Announcement on the Assessment of the ‘Enterprise cloud migration’ in 2017]. http://www.zjjxw.gov.cn/art/2018/2/11/art_1097559_2684.html.

Zhongguo cunchu wang. 2019. Zuixin 2019nian 6yue chaojijisuanji paiming, Top500qiang Zhongguo 219tai, dafu lingxian [The latest supercomputer ranking in June 2019, Top500 strong China 219, a big lead]. http://www.chinastor.com/hpc-top500/061940MH019.html.